Taxation Law Assignment: Case Analysis on Income Tax System & FBT

Question

Task:

Taxation Law AssignmentInstructions and Requirements

Question 1

Alex Limited (a GST registered firm) is planning to have a Christmas party for staff. This party is going to be on the last business day of the year, which is Friday, and the location is planned to be in the restaurant on the ground floor of the office. Staff are allowed to bring only one of their associates and food and drinks are served for free. The number of staff attending this party is going to be 20 people and a total of 40individuals will be served (including the associates).

The estimated cost of the party is $7,480 for the current tax year 2019-2020.

Explain in detail using relevant tax laws and cases whether this cost of $7,480 is deductible for Alex Limited.

Kindly use the four sections of:

1. Facts of the scenario

2. Relevant laws and cases

3. Application of laws and cases

4. Conclusion

QUESTION 2 -

Calculate Total Assessable Income, Taxable Income, Tax Liability, Medicare Levy and Medicare Levy Surcharge, if applicable, for the tax payer (Judy) with information below:

• Judy is a resident married, with no children, tax payer of Australia for the tax year 2019-2020

• Her Taxable Salary earned is $100,000 while her husband’s taxable income for the same year is $150,000 (Including tax withheld) both having no private health insurance.

• Judy has a student loan outstanding for her previous studies at University Technology Sydney of $80,000.

• Judy’s and her husband’s employers pay superannuation guarantee charge of 9.5% on top of their salary to their nominated funds.

• Judy earned a passive income of $20,000 from the investments in shares in the same tax year.

Answer

Answer 1

1. Facts of the scenario –Based on the information given in this taxation law assignment, the employer (Alex Limited) has extended meal & entertainment benefit for the staff members in the form of a Christmas Party. This was held in a restaurant located within the office premises. A total of 20 employees were invited along with their associates thereby resulting in 40 members attending the party. The total cost of the party inclusive of GST has been estimated to be $7,480. The key legal issue is to determine the potential deduction which the employer (Alex Limited) can claim on the amount spent on party i.e. $7,480.

2. Relevant laws and cases- Non-cash and personal benefits which are provided to employees by employers are referred to as fringe benefits. The key examples include employer owned car for personal use, interest free loan, free meals at special occasions or housing benefits. The relevant law for the taxation treatment of these benefits is Fringe Benefit Tax Assessment Act, 1986 (Cth). As per this, the taxation burden for the fringe benefits tends to fall on the employer only. The employees who are the recipient of these fringe benefits do not have to bear any tax burden (Woellner, Barkoczy and Murphy, 2020).

One of the key categories of employee benefits corresponds to meal entertainment. If the employees along with their associates are given meals and drinks on special occasion such as Christmas, this could be referred to as meal entertainment benefit. The key aspect is that these benefits should not be extended during working hours and also must be held outside the normal business premises. This increases the chances of the benefits to be included under the entertainment and meal benefits (Gilders et. al., 2016). As per s. 58P, FBTAA 1986, if the taxable value of the fringe benefit extended to each employee is less than $300, then the underlying benefits are not considered to be fringe benefits and therefore exempted from application of FBT (Austlii, 2020). Also, it is noteworthy that for entertainment related expense, if the underlying expense is deductible, then the employer would also be eligible to claim input tax credit to the same extent as the GST paid. However, no GST input credits would arise for entertainment expenses which are non-deductible (Deutsch et. al., 2015).

As per s. 8-1 ITAA 1997, all outgoings and expenses which have sufficiently close nexus with assessable income production would be tax deductible. It is imperative that these expenses should not be personal but business related. Also, the expense must not be capital in nature and should not relate to production of assessable income (Woellner, Barkoczy and Murphy, 2020). However as per s. 32-5 ITAA 1997, any entertainment expenses incurred by the taxpayer are not deductible under s. 8-1. This has also been indicated in the verdict of Amway of Australia v Commissioner of Taxation (No 2) 2003.There are some exceptions to this which have been highlighted under subdivision 32-B ITAA 1997. One of the relevant exceptions is that deduction under s. 8-1 is permissible for entertainment expenses if they are categorised as fringe benefits. However, if the underlying fringe benefit is exempt, then the underlying benefit provided by the employer would not be tax deductible (Gilders et. al., 2016).

3. Application of laws and case- In the given scenario, it is known that there is a Christmas party which is being held not in the office but in the restaurant located within the office building. Also, the party would serve free food and drinks. Further, the employees have been permitted to bring their associates to the party as well. Clearly, the above description indicates that the money spent by the employer (i.e. Alex Limited) would be categorised as entertainment meal benefits. The important aspect with regards to deductibility of this expense is whether the given benefit is a minor benefit or not.

Total estimated cost of the party = $7,480

Total person present at the party = 40

Expense per person = ($7,480/40) = $187

From the above computation, it is apparent that the entertainment fringe benefit extended to each person is less than $300. As a result, this benefit would be termed as minor benefit. As per s. 58P, no FBT would be payable by the employer since minor fringe benefit exemption would be available.

With regards to deduction of the amount sent by the employer, this will not be possible since s. 32-5 ITAA 1997 prohibits deduction under s. 8-1 ITAA 1997. Further, the exemptions would also not apply since the entertainment fringe benefit provided in this case falls under minor benefit exemption. Since no FBT is levied on the entertainment benefits extended by the employer, hence the input tax credits on the GST paid on the party amount cannot be claimed while filing BAS.

4. Conclusion- It can be concluded that the amount spent by Alex Limited on the Christmas party would not be deductible for tax purposes. This is because it is entertainment benefits and falls within the minor benefit exemption. Further, the input tax credits cannot be claimed by Alex Limited on the GST amount for the Christmas party.

Answer 2

The objective of the given task is to determine the tax liability (including surcharge and offsets) for resident taxpayer Judy for the year 2019-2020.

Computation of assessable income

There are two main sources of assessable income for an individual taxpayer namely the ordinary income as per s. 6-5 ITAA 1997 and statutory income as per s. 6-10 ITAA 1997. One of the most common sources of assessable income is the income from employment. This is considered to be ordinary income and hence assessable as per s. 6-5 ITAA 1997. With regards to taxpayer Judy, the gross annual salary from employment before deduction is $100,000.

Also, it is known that Judy has also derived a passive income on investment to the extent of $20,000. This could potentially be in the form of dividends. Dividend income has been listed as a source of statutory income and hence would be considered to be assessable income. It has been assumed that the dividends are unfranked since no information on franking has been provided. As a result, franking credits have not been considered for this computation. If the dividends were infact partially or fully franked, then franking credits would be added to the assessable income and later provided as deduction from the tax payable.

It is also noteworthy that even though the employer is making a contribution to superannuation for employee Judy, this amount would not be relevant for assessable income computation since this amount is exempt from tax.

Hence, total assessable income for July for 2019-2020 = $100,000 + $20,000 = $120,000

Computation of Total Taxable Income

The relevant formula for computation of taxable income is as follows.

Total taxable income = Assessable income – Tax deductions

The assessable income for taxpayer Judy has already been computed in the previous section. With regards to potential deduction, one potential option is the super guarantee charge or SGC. SGC is paid by the employer as an interest to the relevant tax authorities owing to failure on the part of the employer to fulfil the super payment obligations towards the employees. This amount has no relevance for the employees since this is paid to the ATO (Australian Taxation Office) and hence the employees do not derive any financial benefit from this payment.

Another potential option is the student loan repayment under the HELP program. However, as per ATO ID 2005/27, the amount paid as HELP repayment is not deductible under s. 8-1 ITAA 1997. As a result, any amount which Judy pays in student loan repayment would not be deductible.

Hence, total taxable income = $120,000 - $0 = $120,000

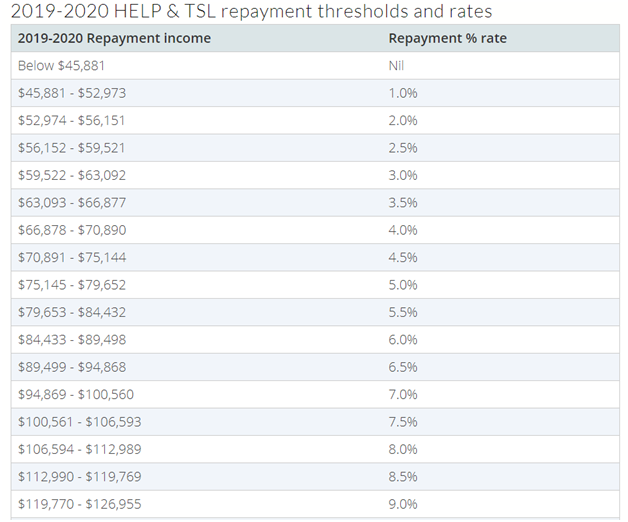

Computation of HELP repayment amount

The relevant HELP repayment and threshold rates for 2019-2020 is indicated as follows.

Source: https://atotaxcalculator.com.au/help-debt

The taxable income for Judy is $120,000. Hence, considering the above table, the applicable repayment % rate for Judy on education loan would be 8.5%.

Current outstanding HELP loan for Judy = $80,000 Amount of HELP repayment for 2019-2020 = 8.5%*$120,000 = $10,200 Clearly, since the HELP repayment for 2019-2020 is lesser than the loan outstanding, hence Judy would need to make a payment of $10,200 towards her outstanding loan taken for her previous studies at UTS.

Computation of Medicare levy

Considering that Judy is a Australian tax resident and does not has any critical medical conditions, she would not be exempted from Medicare Levy. The Medicare Levy is paid at a flat rate of 2% of the taxable income. However, Medicare levy reduction is available for individuals and families belonging to the low income group. For the tax year 2019-2020, if an individual has a taxable income not exceeding $28,501, then reduction in Medicare levy would be available. For family comprising of taxpayer and his/her legal spouse, the threshold income below which Medicare levy reduction could be availed is $48,092. Considering that Judy’s own taxable income is $120,000 for 2019-2020, hence she is not eligible for any reduction in Medicare levy.

Medicare Levy applicable on taxpayer Judy = (2/100)*$120,000 = $2,400

Computation of Medicare Levy Surcharge

The Medicare Levy Surcharge (MLS) is applicable on those Australian resident taxpayers who tend to have income over the threshold level and also do not have private insurance. It is known that Judy and also her husband do not have any private insurance.

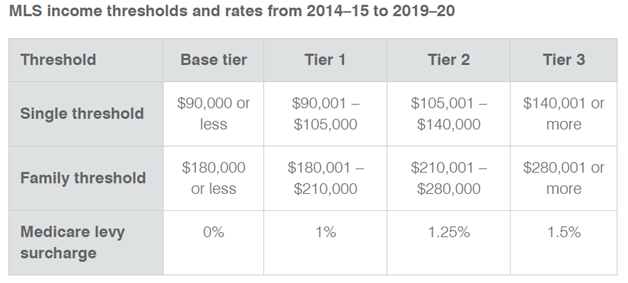

Also, the relevant MLS thresholds which would be applicable for 2019-2020 are indicated as follows.

Source:https://www.ato.gov.au/individuals/medicare-levy/medicare-levy-surchargeincome-thresholds-and-rates-for-the-medicare-levy-surcharge/

Judy has the option of looking at individual threshold and also at the family threshold. Considering the single threshold and her taxable income of $ 120,000, she would fall in Tier 2 with a MLS rate of 1.25% of the taxable income. If she decided to opt for family threshold, then the joint taxable income for Judy and her husband would be $120,000 +$150,000 = $270,000. The family income would also lie in Tier 2 only. Hence, irrespective of single or family threshold, the MLS rate applicable is 1.25%

Hence, MLS for taxpayer Judy =

(1.25/100)*$120,000 = $1,500

Computation of Total Tax liability

The relevant formula for total tax liability is as follows.

Total tax liability = Basic income tax + Medicare Levy + MLS

Taxable income = $120,000

Basic income tax based on applicable tax slabs for resident individual

taxpayers for 2019-2020 = $20,797 + 0.37*($120,000 - $80,000) = $35,597

Total tax liability for Judy = $35,597 + $2,400 + $1,500 = $39,497

Computation of Net Tax liability

Net tax liability = Total tax liability – Applicable offsets

The only applicable offset would be low and middle income tax offset.

Considering the taxable income of $120,000, the low and middle income tax offset applicable for Judy = $1,080 – 0.03*($120,000-$90,000) = $180

Hence, the overall computation is summarised below.

|

Particulars |

Amount |

|

Salary (s. 6-5 ITAA 1997) |

$100,000 |

|

(+)Passive income (s. 6-10 ITAA 1997) |

$20,000 |

|

Assessable income |

$120,000 |

|

(-) Deductions |

0 |

|

Taxable income |

$120,000 |

|

Basic income tax |

$35,597 |

|

(+) Medicare Levy |

$2,400 |

|

(+) MLS |

$1,500 |

|

Total tax liability |

$39,457 |

|

(-) Income offset |

$180 |

|

Net tax liability |

$39,317 |

|

Year 1 |

Year 2 |

Year 3 |

|

|

EBIT |

150 |

180 |

200 |

|

Capital Expenditure |

50 |

75 |

85 |

|

Depreciation |

25 |

30 |

30 |

For the above computation, it has been assumed that the tax withheld is zero.

References

Austlii 2020, FRINGE BENEFITS TAX ASSESSMENT ACT 1986, Available from http://classic.austlii.edu.au/au/legis/cth/consol_act/fbtaa1986312/

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. 2015, Australian tax handbook 8th ed., taxation law assignmentPymont: Thomson Reuters,

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. 2016, Understanding taxation law 2016, 9th ed., Sydney: LexisNexis/Butterworths, Woellner, R., Barkoczy, S., and Murphy, S. 2020, Australian Taxation Law 2020, 2ndedn, Melborune: Oxford University Press