Categorization Of Assessable Income And Income Tax Calculations

Question

Task: A discussion on assessable income and its components with reference to some examples.

Answer

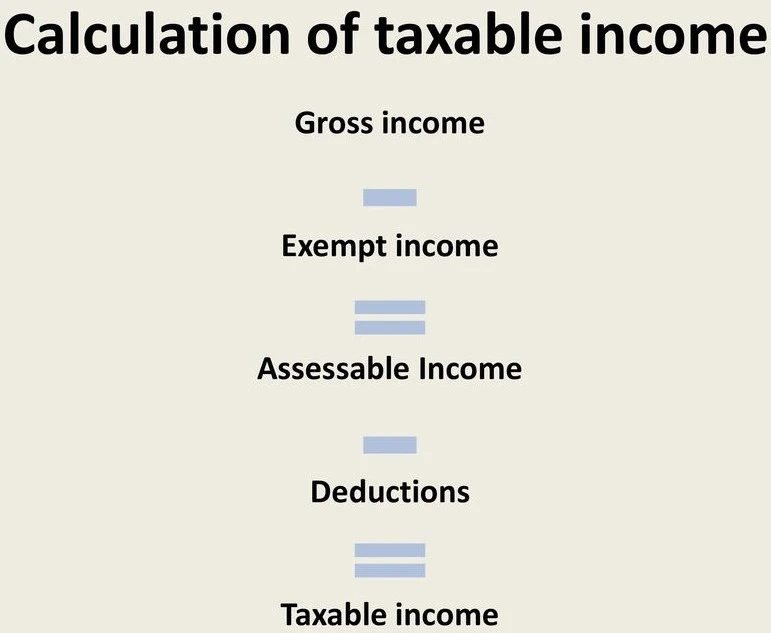

Define the term, assessable income

Assessable income is referred to the total or entire income of a person after certain acceptable deductions has been made. These deductions include expenses incurred in the business, expenses incurred on employment and donations. In other words assessable income is an income which can be taxed by the government for e.g. wages and salary, gratuities, interest arising from bank accounts, dividends and income from different investments, bonus, commission, pension, rent received, etc. If someone is being paid through cash then such income will be assessable (Australian Taxation Office, n.d).

What are the components of assessable income?

The assessable income of a person consists of the following:

- Salary and wages: Salary and wages are one of common forms of income being paid to the employees for the services being delivered by them. The payment can be paid in the form of weekly payments, fortnight or monthly payments, in the form of commissions or bonuses, money paid for part time services or for the casual work, payment provided for parenting leaves, payments received from the policy for income protection, payment received from some insurance policy from accident or sickness or payment received in the form of scheme for workmen compensation (Australian Taxation Office, n.d).

- Other forms of employment income and allowances received: There are some other forms as well through which payment to the employees can be made for the services being delivered by them like, allowances paid for the car services, for travel services or for clothing and laundry services. Payments made in the form of tip, gratuity or payment made for any other service will be considered as an assessable income. Any payments made in the form of consultation fees or any service provided voluntarily. There are some other forms of payment as well like the fees paid to the jury for their attendance. If a person has received an allowance for the expenses incurred during travel or expenses incurred on meal and the same has been paid under the Industrial Law or under any other agreement, then such payments are not required to be included if it did not reflect on the payment summary or it does not meet the reasonable amount or all the expenses were made on deductible expenses (Australian Taxation Office, n.d).

- Interest: In Australia the resident employees receive an interest and the same must be declared as an income. The interest may include any interest that has been earned from the financial institutions or from term deposits, the interest which has been earned from the children’s saving account which is being operated by the employee and not the child, interest which is being paid or credited by the Australian Tax Office, any bonus received in the form of life insurance, or any interest that is being paid from foreign sources (Burton, 2018). Every interest mentioned will come under assessable income.

- Dividends: Dividends can take the form of monetary payments or in the form of shares. If a person is being paid or an amount is being credited in the form of bonus shares then it is necessary for the company which has issued the shares to provide a statement which will indicate that the shares will be treated as dividends. A dividend is commonly paid by a company which is listed as an investment company, a company which is into trading in the form of public trust, a company which is a corporate trust and a company which is limited by trust (Burton, 2018).

- Income from investment trusts: If an income is being generated through investment trusts then the same needs to be mentioned while filing the tax return. Such income or a credit can include any payments from the management of cash trust, money trust, mortgage trust or unit trust. Some income is also managed from certain trusts in the form of property, share, equity, growth, imputation or balanced and these will come under assessable income.

- Rent: Any rent received from a property should be mentioned while filling the tax return. The rent includes income received on properties located in and outside Australia.

- Capital gains: Any income that is being received as a profit or as difference in the form of capital gains should be mentioned while filling the tax return. When there is a difference between the cost of the asset that one has paid at the time of buying it and what one receives at the time of selling it, comes under capital gains (Burton, 2018). Capital gain can also be made a payment is being made by a managed fund. The capital gain is considered as a part of the total income and it is not taxed separately.

- Payments made in lump sum: There are two situations wherein a person receives a lump-sum amount, one when a person is leaving an organization then he is paid an amount for the unused leaves. Second is the payment which is received in the form of arrears which was to be paid for the previous year. These payments are taxable in the same year in which a person receives it and it comes under assessable income.

- Reporting of fringe benefits and compulsory super contributions: There are some other forms of income related to employment as well like reporting of fringe benefits provided by the employer like giving an office car to be used for private purposes or giving a loan at a cheaper interest rate or providing free health insurance for private purposes. If there is a super contribution being made by the employer then the same will come under assessable income (Burton, 2018). It is not required to pay a tax on the payments highlighted previously rather it is used to decide whether a person is eligible to enjoy certain government benefits and relaxation in tax or not.

- Income received through business partnership and trust: The total income which is received in the form of carrying out different business structures will be considered as an assessable income and the same is to be indicated while filing a tax return.

- Income received when running a business individually: If a business is being run by a single person then the income made from the business needs to be indicated while filling the return by using a different business schedule. It is not necessary to file the tax separately rather the filing can be done through one return.

- Income generated through partnership: A business based on partnership is not required to pay any tax on its income rather it has to file a partnership tax return in order to declare its income earned and the expenses which were deducted. The return has to showcase the income and loss being distributed between all the partners (Boccabella, 2013). All the partners are required to declare their share of profit or loss made by them in the personal tax return and it is not necessary that the profit or the income has been actually received by them.

- Income received from trust: A trust is not required to file a tax return but the trustees are supposed to file a tax return on behalf of the trust. It is seen that the beneficiary of a trust makes a declaration about the income that they receive from the trust and the same is considered as an assessable income. If a beneficiary has not received an income still he needs to file a tax return. If the trust is run by a family and the tax has been paid in the form of family trust distribution then it is not required to individually declare the income from the trust (Boccabella, 2013).

- Income received in the form of foreign payments: In case of an Australian resident, he or she needs to declare all the incomes being received by them either from Australia or from any other country. It is necessary to declare all the income that is being received from a foreign country while filling a tax return. These incomes include pensions or annuities, received income from foreign employment, income from foreign investment, income from foreign business and income from capital gains on assets placed in foreign country (Cooper, 2018). There is a possibility of double taxation of the same payment, one in the country from where it is being made and one in Australia where it is being received and is to be considered under assessable income. To save a tax payer from double taxing, Australia has signed up certain treatises and agreements with different countries in the form of credits and exemptions. If a person is a non-resident then he or she is to pay tax on the income received by them from Australia and not from any other foreign country. So it is not necessary to declare any such income that a non-resident receives from outside Australia while filling a tax return and the same does not come under assessable income (Cooper, 2018).

- Other incomes: There are some other incomes as well which a person needs to declare while filling a tax return which has been mentioned below:

- Compensation or insurance paid in case of loss of salary or wages: If a person is being paid for the lost salary or wages under any income, sickness, accident protection law, etc. he or she needs to make a declaration about the income while filing a tax return. If a case has been registered for some personal injury and the person receives lump sum money after the case settles, such incomes are not taxable and cannot be considered as an assessable income once all the conditions have been met (Burton, 2018).

- Shares paid under employee share schemes: If a person engages in an employee share scheme and receives a share at a discounted rate then such discounts are to be declared by the person while filing a tax return. Treating the discounted shares as an assessable income depends upon the type of scheme that has been entered into.

- Awards and prizes: If a person receives a payment in the form of an award or prize then the same has to be declared while filling the tax return. These prize or award may come in the form of winning a lottery amount being run by a bank, or by the building in which he or she is residing, or by the society, credit union or any other body making investment. The prize may take the form of cash or in the form of lower or no interest rates on a loan sanctioned, sponsored holidays or delivery of a car (Boccabella, 2013). It is not necessary to include the prize amounts of an ordinary lottery which is drawn by lotto draws or by raffles. In case a person has won a game show then the amount received needs to be declared while filing a tax return. In case a person sells or disposes off a property which was received in the form of a prize from a lottery and capital gain is made by selling the same then the amount gained should be indicated while filling the tax return and it comes under assessable income.

Question/ Answer Session!

Questions 1):

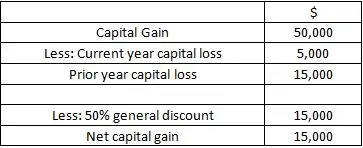

A tax payer in a financial year had a capital gain of $50,000 by selling a land. There was a capital loss of $5000 while selling the shares. There was a capital loss in the previous year as well which has been carry forwarded to the present year which was $15000. The discount method of capital gains tax has been used to calculate the total capital gain. State the assessable total capital gain for the present financial year.

- $15,000

- $30,000

- 7,500

- $22,500

Answer: Correct answer is (a)

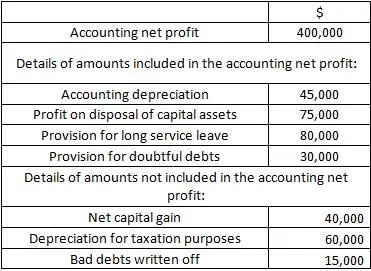

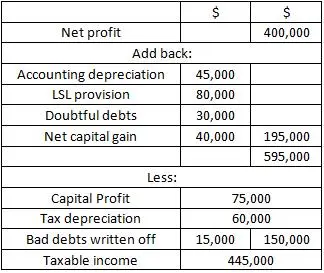

Question 2) Smart Electronic System (SSE) is a private company and it has provided the below information for the current income tax year:

What is the taxable income of Smart Electronic System (SSE) in the financial year?

- $520,000

- $445,000

- $460,000

- $250,000

Answer: Correct answer is (b)

Question 3) One of the trustee of ABC trust made a distribution of $20,000 to Bon Jane. Bon Jane is mentally unstable and is entitled to distribution.

Select one of the statements which accurately reflect the beneficiary status:

- Bon Jane is entitled to share the net income of the trust

- Bon Jane is entitled to share the net income of the trust taking an exception under legal disability

- Bon Jane is not entitled to any share

- Bon Jane cannot have any distribution from the trust.

Answer) Correct answer is (b)

Bon Jane as a beneficiary is entitled to all the incomes being earned by the trust irrespective of the legal disability. Any income earned will be treated as an assessable income. He would be responsible to pay taxes through the trustee.

Reference List

Australian Taxation Office. (n.d) What is income. Retrieved from: https://www.ato.gov.au/Individuals/Lodging-your-tax-return/In-detail/What-is-income-/

Boccabella, D. (2013) What Should Be the Timing Rule for Derivation of Assessable Income by Beneficiaries of Discretionary Trusts? Retrieved from: https://heinonline.org/HOL/LandingPage?handle=hein.journals/jouaustx15&div=5&id=&page=

Burton, M. (2018). Interpreting the Australian Income Tax Definition of Ordinary Income: Ritual Incantation Or Analysis, When Examined through the Lens of Early Twentieth Century Linguistic Philosophy? Retrieved from: https://heinonline.org/HOL/LandingPage?handle=hein.journals/ejotaxrs16&div=5&id=&page=

Cooper, G. S. (2018) The Curious Reform of Foreign Source Income. The Tax Specialist, 22, pp. 2-14.

Get Top Quality Assignment Help and Score high grades. Download the Total Assignment help App from Google play store or Subscribe to totalassignmenthelp and receive the latest updates from the Academic fraternity in real time.