Corporate Accounting Assignment Analysis For Seafarm Group And Woolworths Ltd

Question

Assessment task

Select two public limited companies listed on the Australian Securities Exchange (ASX) that are in the same industry. Go

to the website

of your selected companies. Then go to the Investor Relations section of the website. This section may be called, “Investors”, “Shareholder Information” or similar name.

In this section, go to your companies’ annual reports and save to your computer your firms’ latest annual reports consecutively for last three years. Do not use your companies’ interim financial statements or their concise financial statements. Please read the financial statements (balance sheet, income statement, statement of changes in owner’s equity, cash flow statement) very carefully. Also please read the relevant footnotes of your companies’ financial statements carefully and include information from these footnotes in your answer.

You need to do the following tasks:

OWNERS EQUITY

- From your companies’ financial statements, list each item of equity and write your understanding of each item. Discuss any changes in each item of equity for your firms over the past year articulating the reasons for the change.

- Provide a comparative analysis of the debt and equity position of the two firms that you have selected.

CASH FLOWS STATEMENT

- From the financial statement of your chosen companies, list each item reported in the cash flows statement and write your understanding of each item. Discuss any changes in each item of cash flows statement for your companies over the past years articulating the reasons for the change.

- Provide a comparative analysis of your companies’ three broad categories of cash flows (operating activities, investing activities, financing activities) and make a comparative evaluation for three years.

- Also provide a comparative analysis of the two companies that you have selected explaining the insights that you can get from the comparative analysis.

OTHER COMPREHENSIVE INCOME STATEMENT

- What items have been reported in the other comprehensive income statement for each company?

- Why have these items not been reported in Income Statement/Profit and Loss Statements?

- Provide a comparative analysis of the items shown in the other comprehensive income statement section for the two companies. If these items were included in the income statement / profit and loss statements of each company, how would the profit attributable to shareholders of the company be affected?

- Should other comprehensive income be included in evaluating the performance of managers of the company?

ACCOUNTING FOR CROPORATE INCOME TAX

- What are the tax expenses shown in the latest financial statements of the two companies that you have selected?

- Calculate the effective tax rate for both companies that you have selected. Effective tax rate is calculated as (income tax expense / earnings before tax). Which one of the companies has the higher effective tax rate?

- Comment on deferred tax assets/liabilities that is reported in the balance sheet articulating the possible reasons why they have been recorded.

- Was there any increase or decrease in the deferred tax assets or in the deferred tax liability reported by each of your selected companies?

- Please calculate the cash tax amount for both companies using the book tax amount, changes in the deferred tax assets and deferred tax liability (please do your own research for your better understanding of these concepts and the method of calculating the cash tax amount the book tax amount.)

- Calculate the cash tax rate for both companies. Which company has higher cash tax rate? (Please do your own research to familiarise yourself with how to calculate cash tax rate).

- Why is the cash tax rate different from the book tax rate?

Please remember some aspects of your companies’ treatment of tax can be a very complicated area, particularly for some companies. For a better understanding of the concepts included in the assignment that has not been introduced in the class, please do your own research.

Answer

Executive summary

This report intends to evaluate the financials of two different companies namely Seafarm Group and Woolworths Ltd respectively. The report sheds light on the equity component of the company followed by the income statement, cash flow and other income tax accounting matter. The report further discusses the information about these companies’ equity, comprehensive income statement, statement of cash flow, and corporate income tax accounting tax. To analyse these details thoroughly, the annual report of these companies has been taken into account, and the financials are assessed to observe any variations or alterations in these previously mentioned books of accounts. In addition to these factors, the notes and footnotes to the financial statements of the company have also been taken into due consideration for better understanding. Overall, this report can assist in reflecting enhanced information and comparison betwixt the companies.

Introduction

This report plays a primary role in assessing the details of Seafarm Group and Woolworths Ltd respectively. To Woolworths Ltd, the company has a diversified range of affairs and is also listed on the Australian Stock Exchange. It is a significant player in the Australian retail industry. The reach and availability of the market is high in several segments like gaming pokers, hotel, and liquor.

Nevertheless, the base of customers has been stretched to more than three thousand, and therefore, the company is also regarded as the second largest about revenue. In contrast to this, Seafarm Ltd is primarily an agriculture-based company that is associated with the selling of high-quality seafood and is also registered as a public company of Australia. Furthermore, the company has been involved in several kinds of aquaculture affairs, and it has segregated its issues into three primary segments (Seafarms Group Limited, 2017). Further, last part of the organization is linked to prawn production like black tigers and banana that is sold in the name of Crystal Bay Prawns.?

Owners’ equity

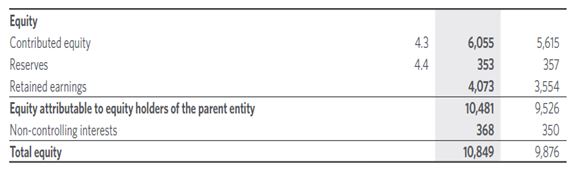

i.) It can be seen from the annual report of Woolworths Ltd that its net equity for 2018 reported at $10849 million when compared to $9876 million in the year 2017. The reason behind this can be attributed to the fact that there are several equity constituents in the company’s financials and the same can be observed from the following table extracted from the annual report. Besides, the company’s contributed equity has also witnessed an increment owing to the issue of fresh shares by it under the program of long-term employee incentives and reinvestment strategies. Moreover, it can also be seen that the reserves have witnessed a decline because of share-based payment costs. Lastly, the alterations in non-controlling interests and retained earnings can be because of enhancement in the company’s net profits even after the dividend payment that was facilitated or undertaken for the shareholders.

In contrast to this, when it comes to Seafarm Ltd, it can be observed that the company’s net equity has witnessed a decline from $327,186,20 in the year 2017 to $158,428,03 in the year 2018 that is a massive deterioration and a negative indicator as well (Seafarms Group Limited, 2017). The fall is observed owing to the alterations in the segment of equity and is further portrayed in the extract from the annual report. Moreover, it can be observed that there has been an increment in the contributed equity and the reason behind this can be attributed to the fact that there was issue of share capital. Furthermore, the retained earnings have depicted a negative figure because of accumulated losses from the past tenures. Besides, there has been an increment in accrued losses that was $199,472,83 that paved a path for the creation of additional retained losses. Lastly, in relation to reserves, the company has witnessed an increment from the last year owing to performance rights that were issued to the employees. This also included lapsed options, share-based payments, etc in the reserves.

ii.) Based on the above analysis, it can be observed that Woolworths is experiencing a better scenario in comparison to Seafarm ltd when it comes to equity and debt position of the companies. This is because Woolworths has better owned capital resources than the latter and is also additionally funded by more of equity and lesser of debt. In addition to this fact, it can be also observed that the company’s investments have enhanced in comparison to the last year. In contrast to this, even though Seafarm is also financed equivalently by debt and equity, yet its ownership has witnessed a tremendous decline in comparison to the last year (Seafarms Group Limited, 2017). In addition, the company’s debt obligations have also witnessed an increment in comparison to the previous tenure that is a negative indicator. Therefore, the company is not in a better position than Woolworths when it comes to equity and debt position.

Statement of cash flow

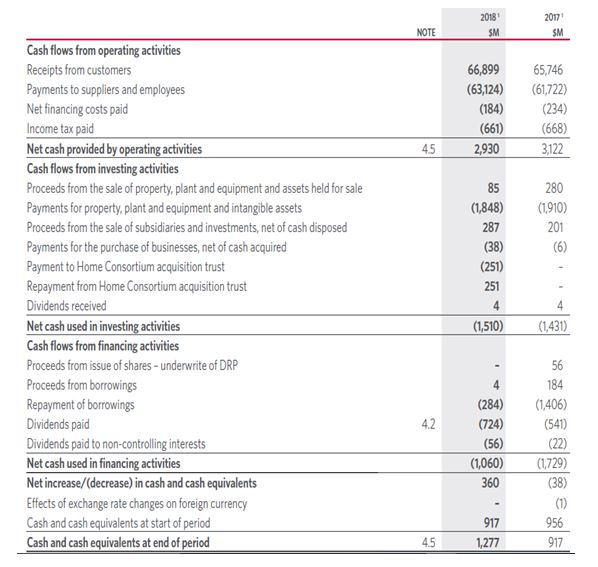

i) It can be seen from the annual report of Woolworths that the company comprises of the following in the cash flow. Firstly, the company’s cash flow from operating affairs comprise of its income and other routine costs that have been incurred during the year. Moreover, this segment has witnessed a decline when compared to the last year and the reason behind this can be attributed to the fact that there have been immense payments to the employees and suppliers in the present year. Secondly, the net cash that have been utilized in the investing activities has witnessed an increment in comparison to the last year. The reason behind this can be attributed to bigger purchases, lesser returns from sale of PPE, etc. Thirdly, the cash utilized in financing activities have been lesser in nature when compared to the last year. Even though there has been dividend increment, yet there has been lesser repayment of obligations in comparison to the last year (Vaitilingam, 2014).

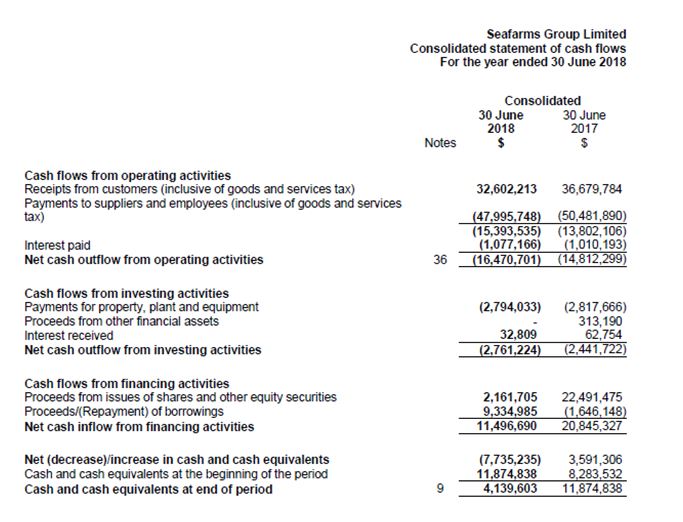

In contrast to the above, when it comes to Seafarm Ltd, it can be seen that there are following segments forming part of its statement of cash flow. Firstly, the company’s cash flow from operating affairs comprise of income and routine expenses that have been incurred during the year (Seafarms Group Limited, 2017). Besides, there has been outflow of net cash and that has enhanced when compared to the last year. Nevertheless, the reason behind this can be attributed to more employee and supplier payments on the company’s part in comparison to customer receipts. Secondly, the company has witnessed an increment in its net cash used in investing activities. The reason behind this is bigger payments for purchase of PPE and nil returns from other financial assets when compared to the last year. Lastly, when it comes to financing activities, the company has witnessed a decline in cash inflow from the same. Even though there has been an immense increase in the liabilities or debts in the present year, yet there has been lesser increase in the returns from the issue of securities and shares. Overall, the net outcome of these activities is that the company has witnessed a decline in its cash and cash equivalent that is a negative indicator.

ii). Comparative analysis

Woolsworth Group Limited: The net cash from operating activities has declined owing to the large payment made to the suppliers and the employees. The reason can be cited owing to huge payment for the business, low proceeds from the PPE in contrast to the last year. When it comes to cash used in financing activities, the cash utilized is low.

Seafarms Group Limited: Cash outflow is observed from the operating activities of the company that enhanced in comparison to the last year due to payments made to supplier and employees. The reasons are due to higher payments for PPE and zero proceeds from other financial assets.

The borrowings has increased to a considerable extent and a small increase in the proceeds from the shares and securities has been noted.

iii). Insight of comparative analysis

Woolworths - Overall, it can be seen that there has been increment in the company’s cash and cash equivalent that indicates better performance and growth in the current year.

Seafarm - Overall, the net outcome of these activities is that the company has witnessed a decline in its cash and cash equivalent that is a negative indicator.

Comprehensive statement of income

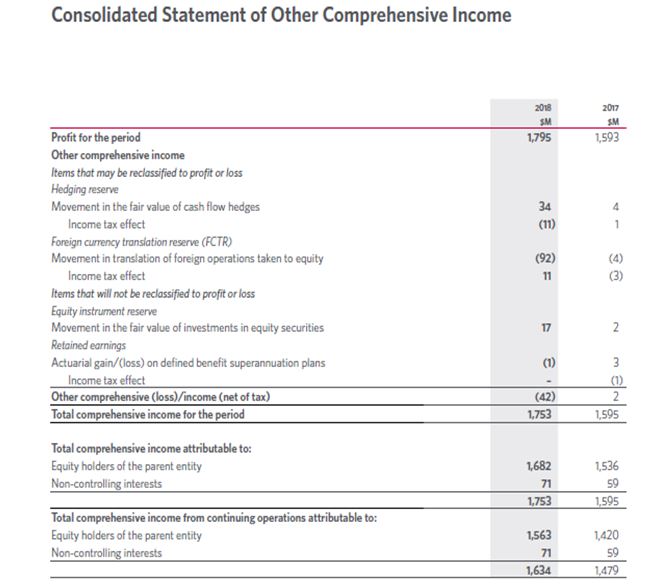

i) vi. There are various items that have been depicted by Woolworths Ltd in its comprehensive statement of income. Firstly, there is movement in equity instrument reserves, secondly there is movement in fair value of income taxes and hedges of cash flows, thirdly there is income tax and translation of foreign currencies thereon, and lastly there is explained superannuation plans losses or gains (Woolworths limited, 2017).

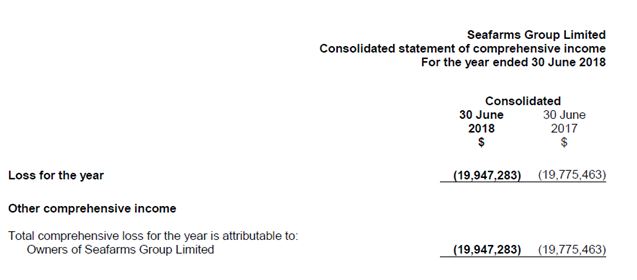

ii) In contrast to the above, Seafarm have not disclosed any details regarding its comprehensive statement of income for the present tenure. This is the reason why nothing is disclosed or reflected in the company’s comprehensive income statement (Seafarms Group Limited, 2017).

iii). The statement of comprehensive income consists of expenses and revenues that have not been realized by the company. Thus, once such transactions are attained, the losses or gains related to the same are identified as realized losses or gains and thereafter, reflected in the income statement. Therefore, the comprehensive statement of income has been alternatively prepared for the sales that have been unrealized in nature (Ross et. al, 2014). Nevertheless, if such income has been reflected in the statement of income, it will reflect that such income which has not been attained has also been depicted in the company’s financials. Moreover, based on the principles of GAAP and IFRS, the total salaries must also be separately disclosed to depict that there are feasibilities of income that can be incurred in the upcoming tenure. However, these must be reflected not inside and instead, outside the statement of income and the reason behind this can be attributed to the fact that such income has not been attained in the present year. In the case of Seafarm Ltd, it can be observed that the company has not prepared or disclosed its comprehensive statement of income during the years. Thus, comparative evaluation betwixt both companies is not feasible in nature.

Moreover, the following items have formed part in the statement of comprehensive income of Woolworths Ltd. Firstly, there is equity instrument reserve that has incurred owing to the revaluation of invested equity securities. In addition, on the disposal of these, the losses or gains attained must be transferred to equity (Power, 2017). Secondly, the company has identified the actuarial losses or gains on the liability of net-defined benefit as and when they occur (Woolworths limited, 2017). Thereafter, these are depicted in the comprehensive statement of income of the company and are not reclassified to such statement of income. Thirdly, the hedge of cash flow is depicted in relation to losses or gains attained based on derivative financial instruments (Porter & Norton, 2014). Lastly, in relation to the variations in foreign currency exchange that has incurred owing to translation of global affairs, planning for the settlement of these transactions have not been made and therefore, have been depicted outside the statement of income.

iv). In relation to the previously mentioned items, if this formed part of the company’s income statement, the attributable profits to the shareholders would decline as a result. The reason behind this can be attributed to the fact that the aggregate impact of such transactions of the company has generated losses and therefore, the shareholders will be the one who are bound to bear such losses. Nevertheless, this would have been an improper treatment because the gains or losses from extraordinary transactions are not so particular as their occurrence. Thus, it is appropriate to reflect these transactions outside the ambit of Statement of Income and instead, report the same in comprehensive statement of income.

The items forming part of the comprehensive income statement are the ones that have not witnessed realization. In other words, it signifies that the company is not aware when such transactions are more likely to incur (Ferris et. al, 2010). However, these transactions can also assist in assessing the future profitability of the company together with its statement of income. For instance, evaluation of comprehensive statement of income can assist in depicting the investment position of the company and how they are able to generate revenues or losses. Therefore, it can be stated that such comprehensive statement of income depicted by the company can play a key role in assessing the company’s performance on a whole but not of the company’s managers.

Accounting for tax associated to corporate income

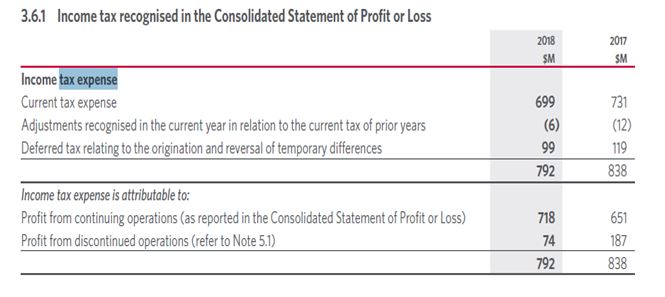

i) x. The tax costs depicted in the company’s financials in the present year are as follows. Firstly, in relation to Woolworths Ltd, the company has depicted its expenses of income tax in its consolidated profit and loss account. Moreover, the same has been reported at $718 million for the current year and in the past year, the same stood at $651 million respectively. Nevertheless, these expenses of income tax have been reflected on the company’s profits from its continuing affairs (Woolworths limited, 2017). In contrast to this, the tax costs on all discontinued affairs profits stood at $74 million for the current year.

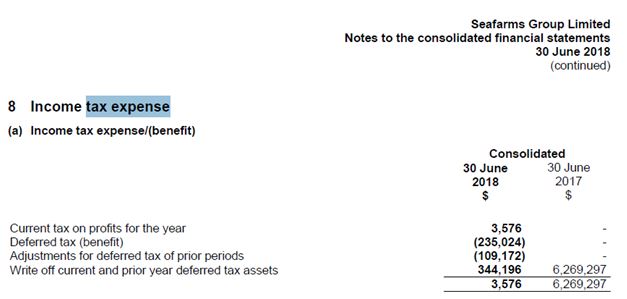

In contrast to Woolworths Ltd, when it comes to the latter company, it can be seen that it has also reflected its expenses associated to income tax in the consolidated profit and loss account (Deegan, 2011). Moreover, the same stood at $3576 as observable from the current year’s annual report.

ii) . Computation of effective rate of tax: The computation of the effective tax rate should be done by dividing the expensed linked with the income tax with the earnings or profit before tax. In relation to Woolworths, its income tax costs stood at $718 million and its profit before tax reported at $2394 million. Thus, its effective tax rate amounts to $718/$2394*100 that gives 30% (Woolworths limited, 2017).

In relation to Seafarm Ltd, its expenses associated to income tax reported at $3576 and its profit before tax cannot be ascertained because there are losses for the year 2018. Therefore, the effective tax rate comes at 30% respectively (Woolworths limited, 2017).

Therefore, it can be concluded that both the companies pursue an equivalent effective rate of taxes.

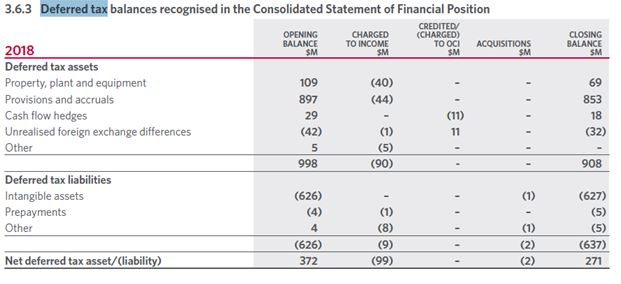

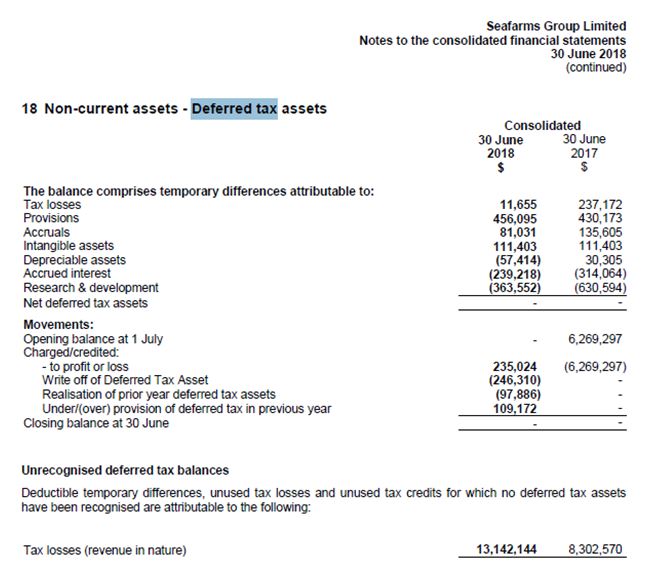

iii). Deferred assets: In relation to Woolworths Ltd, it can be observed that the company’s net deferred assets reported an amount of $271 million in the year 2018. However, the same was $372 million in the last year that means decline in deferred assets in comparison to the last year (Woolworths limited, 2017). Moreover, the computation of deferred tax is done to trace the variations that are temporary in nature between the carrying value of t he assets and liabilities of the company.

In contrast to this, when it comes to Seafarm Ltd, it can be seen that the deferred assets reported by the company stands at zero in the current year. Besides, the same was nil in the previous years as well. Hence, in relation to the same, it is notable that the differences in such amount have been set off by the company in the same tenure itself (Carmichael & Graham, 2012).

iv). Based on the above discussion, it can be noticed that in relation to Woolworths ltd, the company witnessed a decline in its deferred tax assets when compared to the last year. Such decline in deferred tax assets can be because of variations in the permanent and timing differences in relation to both liabilities and assets (Brigham & Daves, 2012). However, in relation to Seafarm Ltd, it can be noted that there has been no variation in its deferred tax assets and the reason behind this can be attributed to the fact that the same was nil in both the years. Nevertheless, in relation to computation of amount of cash tax by utilizing the book tax value, variations in deferred tax assets and liabilities, the following aspects must be taken into consideration:

v). Woolworths Ltd: Total tax provision as reported in the statement of income is ($718million)

Decline in deferred tax assets reported at $90 million

Less- accruals and provisions in DTA ($44million)

Decline in deferred tax liability $11 million

Thus, the amount of cash tax comes at $661m

Seafarm Ltd:

Total tax provision as reported in the statement of income is ($3576)

Decline in deferred tax assets reported at Nil

Less- accruals and provisions in DTA Nil

Decline in deferred tax liability Nil

Thus, the amount of cash tax comes at $3576

vi) Cash rate of tax can be computed by dividing the previously mentioned cash tax by profit before tax. Sea farms will be having the same rate as 30%. However, Woolworths will have an effective tax rate of 27.61% that is attained by dividing cash tax by profit before tax ($661/$2394) *100. Hence, Sea farms has better cash tax rate in comparison to the former.

vii). xvi. Cash tax is primarily paid to government by organizations and is the value that must be reported in the company’s income tax return (Bodie et. al, 2014). Further, book tax is the value of tax that organizations must report in their financials. Besides, these financials are utilized by every stakeholder including lenders, customers, etc to evaluate the company’s performance. In addition, the deferred tax liabilities and assets also form part of a company’s financials that play a key role in the determination of actual payable tax on the company’s part. Overall, for reflecting the true financial position, the company has depicted its liability of income tax in its statements even if the same can be expended in the upcoming tenure. The difference between the book and cash tax arises as the liabilities and the deferred tax assets in combination with the provisions have been framed for the liabilities of income tax that is reported in the financial statements.

Conclusion

Based on the previously mentioned analysis, it can be seen that Woolworths has been performing better than Seafarm and the reason behind the same can be because of its better effectiveness in balancing the debt-equity ratio and other factors as well. Furthermore, since Sea farms has been incurring major losses from the past few years, it is not performing well in its segment and if remedial measures are not implemented soon, it can witness a disintegration path. Moreover, since the company is primarily dependant on debt obligations instead of equity financing, it is negative for the company to thrive in such competitive environment as it can result in hampering the smooth flow of operations. In contrast to this, Woolworths has been relying less on debt and more on equity financing.

References

Bodie, Z., Kane, A. and Marcus, A. J. (2014) Investments. McGraw Hill

Brigham, E. & Daves, P. (2012) Intermediate Financial Management. USA: Cengage Learning.

Carmichael, D.R. and Graham, L. (2012) Accountants Handbook. Financial Accounting and General Topics, John Wiley & Sons.

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Ferris, S.P., Noronha, G. & Unlu, E. (2010) The more, merrier: an international analysis of the frequency of dividend payment. Journal of Business Finance and Accounting. [online]. 37(1), pp. 148–70. Available from https://doi.org/10.1111/j.1468-5957.2009.02174.x [7 April 2018]

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker. Texas: Cengage Learning

Power, T. (2017) Fund choice: Comparing super funds in 8 steps [online]. Available at: https://www.superguide.com.au/boost-your-superannuation/comparing-super-funds-in-8-steps [Accessed 11 May 2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Seafarms Group Limited. (2017) Seafarms Group Limited Annual Report and accounts 2017. [online] Available from: https://seafarms.com.au/wp-content/uploads/2015/02/FY17-Financial-Statements.pdf [Accessed 17 September 2018]

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT Prentice Hall.

Woolworths limited. (2017) Woolworths limited Annual Report and accounts 2017. [online] Available from: http://www.woolworthslimited.com.au/icms_docs/182381_Annual_Report_2015.pdf [Accessed 17 September 2018]