Corporate Accounting Assignment: Discussing Corporate Income Tax Issue For Woolworths

Question

Task: Corporate Accounting Assignment task: Collect the latest annual report of an ASX listed company for the last 2 financial years. Please read the financial statements (balance sheet, income statement, cash flow statement) and notes attached to financial statements on income tax issues very carefully. Please remember some aspects of your firm’s treatment of its tax – can be a very complicated area, particularly for some firms. Based on your understanding of the topic “accounting for income tax” and based on your reading of the collected annual reports, do the following tasks.

i Briefly explain the concepts of accounting profit, taxable profit, temporary difference, taxable temporary difference, deductible temporary difference, deferred tax assets and deferred tax liability.

ii Briefly explain the recognition criteria of deferred tax assets and deferred tax liability.

iii What is your firm’s tax expense in its latest financial statements

iv Is this figure the same as the company tax rate times your firm’s accounting income Explain why this is, or is not, the case for your firm highlighting the reasons for differences.

v Identify the deferred tax assets/liabilities that is reported in the balance sheet articulating the possible reasons why they have been recorded.

vi Is there any current tax assets or income tax payable recorded by your company Why is the income tax payable not the same as income tax expense

vii Is the income tax expense shown in the income statement same as the income tax paid shown in the cash flow statement If not, why is the difference

viii Briefly explain the concepts of temporary difference and permanent difference. Identify any permanent differences that your company may have.

ix What do you find interesting, confusing, surprising or difficult to understand about the treatment of tax in your firm’s financial statements What new insights, if any, have you gained about how companies account for income tax as a result of examining your firm’s tax expense in its accounts

Answer

Executive Summary

Accounting for income tax holds a place of special significance because it is directly related to the profit-earning capacity of the company. The different companies used different concepts of accounting for income tax and hence, open up the area of study. Income tax accounting helps in ascertaining the payment of income tax in the books of accounts and expenses for the period. To prepare the corporate accounting assignment, Woolworths, a retail giant and listed on the ASX is selected for the study. The report is an exhaustive research on the income practice of the company whereby different aspects of the company ranging from concepts of income tax accounting, recognition criteria, deferred tax, and liabilities are discussed. the report comments on the practices of the company in the desired area. The conclusion drawn from the report indicates that the income tax aspect of the company is a little confusing however the same has been supported by conclusive evidence.

Introduction

Accounting for income tax is one of the vital topics as it helps in recognizing the tax liabilities for the estimated income tax payable and ascertains the tax expense for the present period. Income tax accounting helps in the proper recording of income tax in the books and helps to confirm the income tax that accrues for the present period (Harumova 2016). The objective of the report is to project and discuss the corporate income tax issue for Woolworths, listed on the ASX. Different concepts relate to accounting for corporate income tax and hence, require proper discussion for better understanding. Woolworths is selected as it is a pioneer in the retail segment and has intact financial statements. Woolworths was established in 1924 and dominates the retail segment encompassing more than 3000 stores. The company has a wide range of customers exceeding 29 million and can serve them through the presence of more than 205000 employees. Accounting for income tax is discussed in the light of Woolworths whereby the report initiates with the introduction, explanation of different concepts, recognition criteria, tax expenses of the firm, temporary and permanent differences followed by the conclusion.

i. Discussion of various accounting concepts

Accounting profit

Accounting profit is the excess of the revenue in comparison to the expenditure incurred by the company. The amount received from the difference is treated as an accounting profit (Meade 2012). There are two concepts available that is the cash and the accrual system. The company uses more of the accrual system because the transaction should be recorded as and when the transactions take place. For example, the operations of the business have led to a profit of $1000 million by investing a sum of $900 million then the profit will be $100 million.

Taxable profit

After computation of the accounting profit when we deduct unearned income followed by the accrued expenses we derive at the taxable profits. This profit is useful to compute the taxable component of the company (Vernimmen 2017). For instance, if the profit of Woolworths stands at $300 million and due to depreciation the taxable profit comes to $250 million with the tax rate being 30% the profit after tax will be $150 million.

The temporary difference

Some items in the financial are treated on a differential basis that is accounting treatment is different while in case of tax return it differs. The presence of such differences gives rise to a temporary difference (Vernimmen 2017). The rate of depreciation tends to differ when it comes to the accounting treatment and the ones that are witnessed in the financial records.

Taxable Temporary Difference

There appears a timing difference in the financial statement owing to the accounting and tax treatment. The timing difference tends to lower the tax in the present period while escalating the tax in the further years is the taxable temporary difference (Harumova 2016). For instance, as per the accounting function, the rate of depreciation might be $10$ while as per the tax rule it might stand at $12, and hence $2 difference will lower the tax at the present time but will lead to more tax in the further year.

Deductible temporary difference

These are the difference that leads to taxable income on a higher scale and hence the income tax payable is higher in the current year. However, the timing difference needs that the income tax is reduced in the later years. The difference in the timing leads to the creation of the deferred tax asset and tagged as a deductible temporary difference (Harumova 2016). The provision for employee benefits is an apt example of such a difference.

Deferred Tax Liability

It is such a situation where due to the difference in the timing the tax payment for the current period tends to be low while it becomes more for the future. Such a situation exists when the company pays a lower advance tax that increases the future tax obligations of the company (Vernimmen 2017). if the tax liability of the company is $500 while the payment made by the company is $400 then the deferred tax liability will stand at $100

Deferred Tax Asset-

The timing difference might increase the current tax payment while decreases the tax payment for the future then it is referred to as an asset. This is actually happening when the advance tax payment is more as compared to the tax payable. For instance, the advance tax stands at $600 while the company made a payment of $800 then $200 will be the deferred tax asset for the company.

ii. Recognition criteria

Recognition criteria for deferred tax assets and deferred tax liability criteria and the manner for the recognition, measurement, and disclosure for the deferred assets and liabilities has been guided by the AASB 112 on Income Tax. As per the standard, the deferred tax liability needs to be recognized for every temporary difference that is under the tax ambit instead of deferred tax liability happening on the goodwill recognition and the time when the transactions happen; such does not have any impact on the taxable profit or loss (Meade 2012). The difference out of the same and happens to be temporary and taxable leads to an obligation for the payment of tax in the future and hence deferred tax liability is bound to happen. In the case where the carrying amount gets recovered such temporary difference is reversed leading to taxable profit for the organization as a whole. It needs to be noted that the presence of economic benefits leads to tax payments and hence, outflows occur thereby adhering to the guidelines of the deferred tax liability (Abhisekh&Divyashree 2019). Recognition of deferred tax asset needs to be recognized for such difference that comes under the purview of the taxation and such difference can be used for transactions leaving aside the transactions that are not linked to combinations and other transactions that have no relation with the taxable profit or loss

During the course of activity, it is imperative that the deductible amount is reduced later than the period of recognition. Hence, such recovery in the future aspect in the area of tax brings or attracts the current recognition of the deferred tax asset.

On the other hand, where the carrying amount stands lower than the base of tax then such difference attracts deferred tax assets in the present time is linked with the tax amount that will be recoverable in the future.

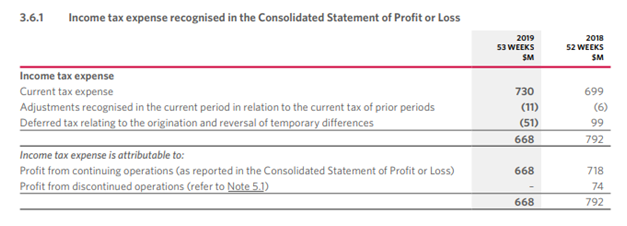

iii. Tax expense of Woolworths

Going by the annual report ending 30th June 2019, it is noted the income tax expense at present stands at $730 million in comparison to $699 million in 2018 (Woolworths. 2019).

(Woolworths. 2019)

The income tax expense of the company comprises of current tax, as well as deferred tax. The recognition of an income tax is done in the income statement. The segregation of the income tax is done as per the table reflected below:

The explanation of the items contained in the financial statements has been properly reflected in the notes to the financial statement. Moreover, the reason pertaining to recognition and non-recognition has been adequately done. The financial position statement comprises of separate items such as deferred tax assets and liabilities and the tax that is required to be paid.

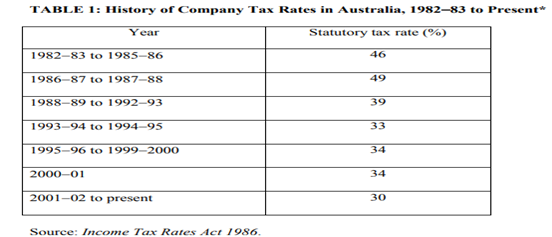

iv. Difference in the tax rates

The present income tax liability of the company is computed through the multiplication of the corporate rate of tax with the taxable profit of the company for every year. The corporate tax in Australia stands at 30%. The tax structure of Australia since 1982 is as follows:

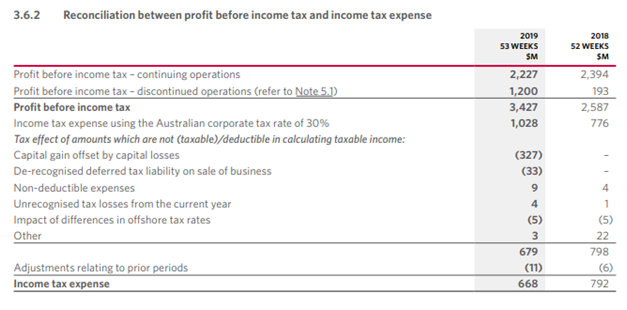

To arrive at the accounting profit there are certain adjustments that needs to be done. As per the information contained in the annual report of Woolworths, there is a link between the accounting profit before tax and the expenses

(Woolworths. 2019)

As per the annual report, the profit that is extracted before the adjustment of income tax stands at $2227 million and the corporate tax rate stands at 30% (Woolworths. 2019). From the details, the income tax expense of the company can be computed that is:

Income tax expense =PBIT multiplied with rate of tax

=2227million *30% = $668 million

The present tax expense projects the tax payable amount by the company to the tax authorities for the profit earned. Hence, the overall adjustments and discussion gives a fair indication that the company has an accounting profit of $2227 million followed by the income tax expense that stands at $668 million

(Woolworths. 2019)

v. Reporting of deferred tax assets and liabilities

The computation of deferred tax assets is done through the balance sheet mechanism; the measurement applies at such rate that needs to settle the specific liabilities that pertains to the future course of action and at the rate that is applicable at the liability settlement time. The deferred tax assets applicable to PPE are recognized in connection with the timing difference pertaining to depreciation between the corporate rate and the taxation process (Woolworths. 2019). Moreover, the deferred tax assets pertaining to provisions, as well as accruals projects the creation of accrual for benefits needed in the future. On the contrary, the deferred tax liabilities pertaining to intangible assets project the payable of liabilities shortly. The advantages from the intangible assets will accrue over the life tenure of the assets hence the carrying value needs to be ascertained utilizing the value in use mechanism. Foreign exchange differences that are unrealized, prepayments, and other deferred tax liabilities occupy a smaller position and the presentation is due to certain movements in the price. (Li et al 2011)On a complete evaluation and reference to the notes to the financial statements, it can be stated that the deferred tax assets are not recognized in consideration of the capital and revenue losses as it is improbable whether the capital and revenue gain will be contained in the future (Li et al 2011). Moreover, recognition of deferred tax assets and liabilities happens when it is applied by the tax department and the Group tends to settle the same.

vi. Current tax assets/income

The details and information regarding the current tax assets or income are generated by the study of the annual report. As per the annual report, the company contains current tax and income tax payable. The same is required to be managed with the losses that arrive from previous years and other items of adjustment. Income tax has two components that are the current tax and the deferred tax. The current tax can be defined as the income tax amount that is required to be paid in consideration of the taxable profit (Potter et al 2019). On the other hand, the deferred tax is the difference between the carrying and actual value of the assets and liabilities.

vii. Income Tax expense

Income tax expense can be stated as the expense amount that the business recognizes in a certain accounting period. The income tax expense does not match with the standard income tax as there are many differences between the amount that is reported (Cheng, Young & Yang 2018).

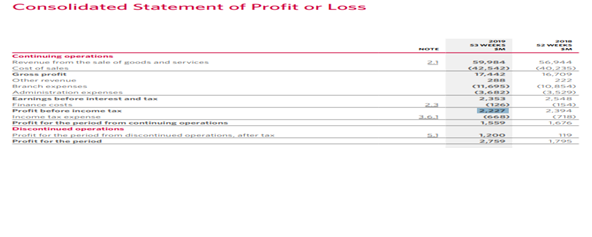

As per the income statements, the projected income tax does not match with the tax paid under the cash flow statement. In 2019, the total income tax expense stood at whereas the income tax that appeared as per the cash flows stood at $774 million (Woolworths. 2019). Hence, a notable difference lies when it comes to the reporting of income tax that is due to modifications like expenses, prior year adjustments of the items, and the subsidiary tax. The accounting profit is needed to be adjusted with the items of income tax expenses and the total payment will be ascertained through it. the payable income tax is adjusted with the expenses pertaining to the income tax while the cash flows contain the tax outflow from the normal accounts. On the occurrence of any deficit or excess payment, the same will be reflected by way of refund or repayable in the cash flow.

viii. Concepts of the temporary difference and permanent difference:

The asset or liability of a company might be recorded at one value owing to the financial reporting process while the same might be recorded at different aspects for tax. The difference arises owing to the policy of taxation that might need the deferral or acceleration of the different items for tax (Romney 2016). Such differences are temporary because the assets will be recovered and the liabilities will be honored and hence the differences will be expelled. The difference that brings a taxable amount in a later time span is stated as the temporary difference whereas the difference that attracts a deductible amount at a later point of time is defined as the deductible temporary difference. The taxable difference is the ones that might alter the taxable amount levied on the assets or the liabilities settlement. Some of the instances where taxable difference happens are the prepaid expenses, capitalization, and amortization of different development costs and rates of depreciation (Abhisekh&Divyashree 2019). The deductible temporary difference is the expenses that are required to be declined when a specific asset is recovered or liabilities settled. Such assets might be led to a decline in the tax expense slab.The permanent differences can be termed as the difference where neither the deferred tax assets, not liabilities are created. The variation happens when recognition of the item of revenue or expenses is done that is required for taxation. Considering different tax laws is the main reason for the difference and such alteration might not consider the revenue item. However, for Woolworths, no differences were noted in the financial statements.

ix. Insights

Going by the entire study, it can be commented that the tax aspect of Woolworths comes under the ambit of both interesting and contrasting. The research indicates that the company can carry forward the losses to the next year and the same can be set off with the future year profits. Losses that were accumulated over the years can be written off with the revenue. The point of contradiction happens concerning the fact that with the generation of revenue the company might not be liable for tax payments. Such observation creates a lot of confusion and difference in the assets and liabilities valuation (Woolworths. 2019). Thereby, inaccuracy can be observed in the final tax liability of the company whereby such differences must be accounted for. From the annual report, it can be seen that the organization is required to ascertain the assets and liabilities at the carrying value. However, the actual BV of the transaction might be different. Another observable fact is the no inclusion of the goodwill in the computation of the deferred tax assets. To ascertain the overall figure, either of the two systems that is the cash or the accrual system might be used. In the case of Woolworths, the accrual system is followed however, the difference can be observed in the area of accrued interest (Woolworths. 2019). The accrued interest is chargeable in the year of accrual however; the receipt date of the accrued interest differs. Furthermore, the analysis provides a clear understanding of the increment in the income tax and other tax expenses and the influence of the impact on the business. Hence, the overall study reflects that a difference or an error might be observed in the forecasted value.

Conclusion

The objective of the report was to conduct in-depth research on the topic of accounting for income tax. The study concerning Woolworths has provided a clear implication of the various elements present in the accounting for income tax. The overall study provides a glimpse that the corporate entities have to follow the statutory laws and hence the difference is witnessed in different items. Moreover, the business has the facility to carry forward of losses that helps the business to set off the losses in the year of profits. The computation of deferred tax assets and liabilities are subjected to different adjustments and standards. Moreover, the tax aspect of Woolworths is interesting, as well as confusing. Another important observation is the accrual system that is subjected to deviations. The overall study provides a glimpse that income tax accounting is a vital concept however arriving at a proper conclusion is not an easy task as there are several adjustments. Thereby, it can be commented that the tax system followed by the Woolworths is confusing as there are plenty of adjustments however the best part of the company si that it has provided complete disclosure.

References

Abhishek, N., &Divyashree, M. S 2019, International financial reporting standards - A tool for harmonising the financial reporting. International Journal of Financial Management, vol. 9, no.1, pp. 41-47

Cheng, Q., Young, J.C. & Yang, H. 2018, Financial reporting changes and the internal information environment: Evidence from SFAS 142, Review of Accounting Studies, vol. 23, no. 1, pp. 347-383.

Harumova, A 2016, The economic function of deferred taxes, Newcastle upon Tyne: Harumova Scholars Publishing. Li, Z., Shroff, P.K., Venkataraman, R. & Zhang, I.X. 2011, Causes and consequences of goodwill impairment losses, Review of Accounting Studies, vol. 16, no. 4, pp. 745-778.

Meade, J 2012, Reporting for reporting entities. Charter, vol. 83, no. 8, pp. 44-45.

Potter, B., Pinnuck, M., Tanewski, G., & Wright, S 2019, Keeping it private: financial reporting by large proprietary companies in australia.Corporate accounting assignment Accounting & Finance vol. 59, vol. 1, pp. 87–113.

Romney, M.A. 2016, Finding the good in goodwill: Evidence from acquisitions using income tax accounting, Michigan State University.

Vernimmen, P 2017, Corporate finance : theory and practice. Fifth edn. Hoboken: Wiley.

Woolworths. 2019, Woolworths 2019 annual report, Available from: https://www.woolworthsgroup.com.au/icms_docs/195582_annual-report-2019.pdf [Accessed 2 June 2020]