Business Economics Assignment Evaluation Of Law Of Supply And Demand & Economic Theories

Question

Task:

You are supposed to prepare a business economics assignment addressing the below tasks in the context of contemporary business economics:

Task 1: Law of supply and demand

Task 2: Compare and Contrast 20th and 21st century

Answer

Business Economics Assignment Task 1: Law of Supply and Demand

1.0 Introduction

In general terms, economics is referred to as the study of producing, distributing, and consuming products and services. The study of economics is separated into majorly two divisions that are microeconomics and macroeconomics. In this view, macroeconomics deals with aggregating economic quantity like national output and income while microeconomics is the study of markets and decision-makers that includes consumers and business owners (Hahn2016, p. 28). The demand and supply analysis is part of a microeconomics study that deals with the interaction of buyers and sellers to determine price and quantities. In market economies that are owned by private enterprises forms chief concerns for investment analysts as supply and demand from the bases of microeconomic tools.

2.0 “Law of Demand” and Changes in the demand curves

2.1.1 “Law of Demand”

To understand the “Law of demand”, it is important for analysing concepts of demands. In this view, the quantities that customer willing to purchase is dependent on the various factors while is backed by purchasing power. Any wish of the customer that is backed by purchasing power is known as demand for the particular commodity or service. Concepts of demands analyses the consumer behavior that changes with alterations in prices keeping other factors constant. The “law of demand” assumes that the increase in the commodity price or service reduces the demand and vice versa keeping other factors like preferences, substitutes constant (Hildenbrand2014, chap 1). This is the reason why sales and discounts offered are a huge hit as customers tend to purchase when the prices are reduced as consumers are considered to be rational.

However, the price of a good is important in determining the willingness of the customer as variables like incomes, tastes, and preferences, prices of the substitute's influences purchasing decisions. The relationship of the aforementioned variables with consumer willingness is captured by the economist as the demand function. The demand function is

Qdx = f(Px, I, Py)

Thus, Qdxis represented asthe demanded quantity of good x where Px is the price, I is the income while Py is the price of another product or substitutes. Thus, it can be said that the price is inversely proportionate to the quantity purchased. This inverse relation occurs due to diminishing marginal utility as the consumer demands more with a reduced price, the price increases while the need for additional units declines. All the quantity demanded at different price levels can be depicted in the same demand curve however, the expansion or contraction of the demand curve depicts changes in other factors.

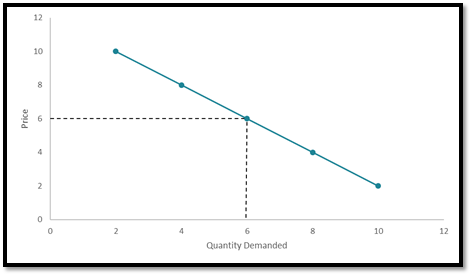

Figure 1: Negatively Downward Sloping Demand Curve

(Source: Hildenbrand 2014, chap 1)

The market demand is negatively downward sloping as the price is inversely related to the quantity demanded. Many economists represent the law of demand as a concave shape while it was some scholars explain it through a straight line. In the given demand curve, the X-axis represents the quantity demanded while the price is determined through Y-axis. The quantity demanded is a bundle of goods that the final consumers are willing to purchase at a particular price.

2.1.2 Exceptions to the law of demand

Giffen Goods

These goods are inferior while lacking the substitutes thus representing a large part of consumer's income. The quantity demand for the Giffen product increases with the price of the products, however empirical results for this exception are rare hence it is mostly viewed as theoretical concepts.

Veblen Goods

The Veblen goods are luxurious products thus indicating the social and economic status of the individual; hence the demand for such products increases with a price hike for showing off wealth and status.

2.1.3 Movements and Changes in the Demand Curve

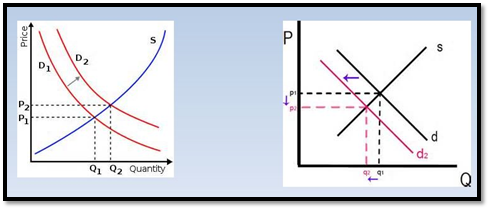

The Law of Demand focuses on the unlimited wants of the people as they try fulfilling urgent wants over less urgent needs. As consumers tend to consume more of the given product, the value of each additional unit reduces thus, adding all the quantity demanded that determine consumer willingness to purchase at a given price. Thus, there is a major difference in “movements along the demand curve” and changes in the “demand curve” (Hildenbrand2014, chap 1). The movements along the demand curve will represent changes in price that reflect changes in “quantity demanded along with the same demand curve”. In this view, modification in the demand refers to a movement of the original demand curve due to change in income, tastes & preferences, price of other substitutes, and other underlying consumer patterns. The “demand curve” moves rightwards when there is an upsurge in demand pattern due to which a new equilibrium of demand and supply is established. On the contrary, the “demand curve” shifts leftwards if there is a decreasing trend with reduced price and quality demanded.

Figure 2: Right and Left shift of Demand Curve (Changes in Demand Curve)

(Source: Hildenbrand 2014, chap 1)

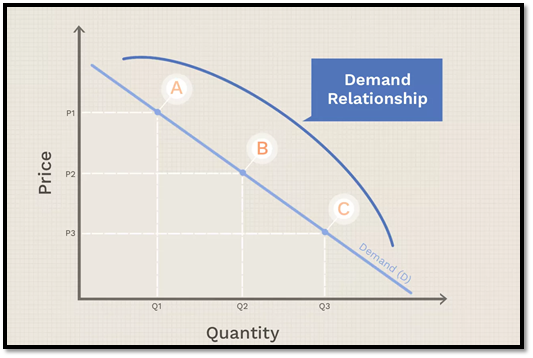

Figure 3: Movement Along the Demand Curve

(Source: Hildenbrand 2014, chap 1)

In the above diagram, point A represents, price of a commodity at P1with the corresponding Q1, similarly at point B, the price of commodity X. Hence, the movement of the demand curve represents different quantities and prices at different points along the same demand curve.

3.0 Law of Supply, Changes, and Movements

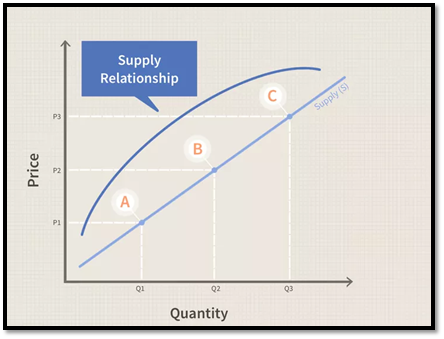

The law of supply represents the microeconomic condition in which all factors are treated equivalent as suppliers can supply more if the price of goods or services is increased. Thus, the price positively related o supply as the suppliers maximize their profits by supplying higher quantities if the prices are enhanced. It can be said that higher prices motivate the producers as higher quantities, which shapes the supply curve in a upward sloping trend which responds to variations in the price during a stipulated period (Marshall2013, chap 2). Thus, the business produces more for receiving high revenues with increased price.

In the given diagram below, the upward sloping supply curve is marked with A, B, and C points that further represent direct co-relation with supplying quantity and prices. Taking Point, A, for example, the quantity supply of commodity X in Q1 with corresponding prices at P1. The reason behind the” upward-sloping supply curve” is that the suppliers contain the flexibility of how much good is to be produced and brought to market. The supplies of sellers are fixed hence; the suppliers and seller face undertake decisions of either selling the stocks or withholding it as the prices are set by consumers. Thus, if the consumer increases the demand for the product, suppliers use multiple resources for the production of products that further increases the overall supply in the market (Marshall2013, chap 2). The law of supply is integrated with the law of demand for explaining the allocation of resources and determination of prices of goods and services.

Figure 4: Upward Sloping Supply Curve

(Source: Marshall 2013, chap 2)

Supply is represented as a function of production costs that include labour and materials that ultimately reflect the opportunity costs. The other product costs relate to available technology that can be combined with inputs, institutional costs along with several sellers with production capacities in a given time frame.

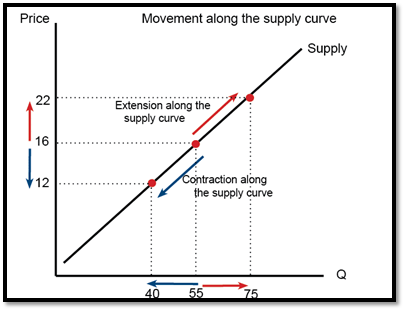

3.1.1 Shifts and Movements in the supply curve

The shifts and movements in the supply curve represent different aspects of market phenomena. Just like the demand curves, the movement along the same supply curve represents consistency. The movement along the supply curves occurs with changes in price level corresponding to modifications in supply changes aligning with the original supply relations. Thus, it can be said that the movement along the same supply curve is determinant of only price changes.

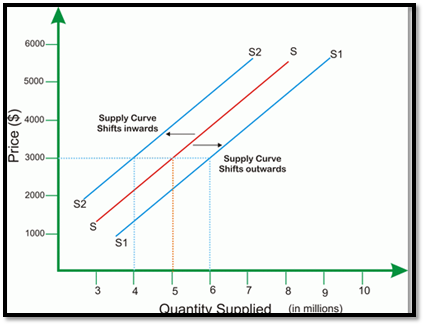

Figure 5: Shiftsin the Supply Curve

(Source: Marshall 2013, chap 1)

Figure 6: Movement along the supply curve

(Source: Marshall 2013, chap 1)

However, a shift in supply curves represents changes in other factors while price remains the same. For instance, if the price of fruit juice bottle is $2 while the quantity supplied decreased from Q1 to Q2 then, the supply curve will shift similarly to demand curves(as per the given diagram above)

The “supply and demand curves” create an “equilibrium price” at which the producer can sell his products while the consumer can purchase at the market-determined price level. Since the supply curve is in “upward sloping trend” and the “demand curve is downward sloping trend”, hence both functions intersect at a point that creates market price and market demand (Marshall2013, chap 2). The equilibrium price is profitable for both the buyers and sellers.

4.0 Conclusion

The Law of Demand and Supply depicts the phenomena of everyday life. Both the concepts consider changes in price while other factors are remained constant thus describing the value of goods and services in context with its price in scenarios when the products are available in abundance or are scarce. The price is inversely related when the “law of demand” is explained while the price is directly related when the “Law of Supply” is discussed. The “Law of supply” and demand is essential as it helps entrepreneurs, agencies, and economists for predicting market conditions.

Task 2: Comparison and Contrasting of 20th and 21st century

1.0 Introduction

Economic Theories helps in understanding the financial development that influences saving behaviours in different ambiguous ways. The economic theories are defined as social sciences that deal with issues of allocation of limited resources for satisfying unlimited human wants.

2.0 Major Economic concepts of 20th century

In the 18th and 19th century, the focus was given on growth and development due to which growth theories, public finance, fiscal measures, international economics was developed. The Harrod- Domar Model was jointly developed by Roy Harrod and Evsey Domar basing their theories on natural rates and warranted rates of growth. Keynes developed an economic model that showed increased incomes generate savings which further results in investment. In this view, taxation and fiscal measures have been prevalent from the 17thcentury till the 21st century determining different aspects of taxes as fiscal policies. In the 1960s (towards the 20th century) microeconomic development took place like cost-benefit analysis that appraises all costs and benefits that determines the distribution of public budget. In the 20th century, the supply side of labour economics was developed that determined various factors like male-female participation, the role of labour unions, and others (Ros2013, chap1). The concepts of human capital like education, training, job opportunities were developed that also became a dominant tool in determining understanding labour economists. The concepts related to the industrial organization (public policies for monopoly, market structure, technical change) and agriculture (as farming in many countries heavily influenced price controls, income supports market cartels) also grabbed the attention of many economists. Public spending was increased to improve public services while major changes were also made in areas like climate and energy due to which many economists elaborated theories like energy economics, environmental economics, and others that integrated basic economics with factors of environment and energy

3.0 Major Economic concepts of 21st century

Major changes in the contemporary theories occurred after the 2009 financial crisis which prompted the economist to consider other aspects while integrating several domains into economic concepts. In this view, Elinor Ostrom won the prize for analyzing the economic governance of common resources like water supplies, fishes, and others. Contradicting Hardin's theory (which focused on that common resources should be completely managed by the government for preventing overuse), Ostrom depicted that the management of common-pool resources can be done effectively through collective methods (Wang2016, chap 1). Behavioral economics is a recent development that is based on the insights on psychological factors that concern factors like human judgment, decision making, uncertainty, and other into economic science (Caron2014, chap 2). Also, concepts like information asymmetry helped in acknowledging the dynamics of markets and why corporate transparency is important. Decision- making the science of individuals was also clearly understood by game theory concepts. This theory exclaimed that the decision making of an individual is assumed on expectations of reactions or behaviours of other participants.

3.0 Compare and contrasting

From the 18th to 20th centuries economic models like classical economics, neoclassical theories, Keynesian economics, and many others for evaluating different aspects of the market and monetary aspects. However, in the 21st century, several new concepts were involved in global economics, behavioural patterns, and others. The modern economic theory is categorized into policy and politics. The ideas of scholars that dealt with the politico-economic paradigm encompassed political and economic goals to understand the functions of economics and societies (Hilton et al 2013, chap 2). Post World War 11, economic growth and rising incomes constructed social democratic consensus which also led to the targeting of full employment level by Keynes that was also considered basic indicators of economic success. In addition to this, the breakdown of international monetary systems led to constructing phenomena like stagflation that contradicted the Philips curve.

4.0 Relating Economic Theories Business Practices

In real-time scenarios understanding consumer behaviour, structure, and reasons behind government policies, market dynamics, use of resources are important to any business units. Thus, various concepts pointed out by economists helped in drafting government policies, changing market conditions, incorporating sustainable and transparency practices have shaped the core structure of economies. In this view, the theories developed in the 18th and 19th century was developed through the mere assumption that had no or little evidence for practical applications. Also, concepts like costs and profits are differently understood by economists and business managers as the former calculate opportunity costs while the latter evaluate only explicit costs.Several economic forecasting concepts like cost elasticityof demand, cost output relations, promotions, and elasticity are considered for forecasting market conditions.

5.0 Conclusion

The economic theories relate to microeconomic and macroeconomic branches in the 20 and 21st centuries. In the late 1900s and 2000s, the majority of the governments were centre led thus following a social democratic approach. Managerial economics in recent times considers collaboration of various viewpoints for undertaking decisions and future planning of the business units. The demand and supply analysis is part of a microeconomics study that deals with the interaction of buyers and sellers to determine price and quantities. In market economies that are owned by private enterprises forms chief concerns for investment analysts as supply and demand from the bases of microeconomic tools.

Reference List

Caron, F2014, 'An economic history of modern France,' Abington, Routledge, chap 1.

Hahn, R & Metcalfe, R2016, The impact of behavioral science experiments on energy policy, Economics of Energy & Environmental Policy, vol. 5, no. 2, pp.27-44.

Hildenbrand, W 2014, 'Market demand: Theory and empirical evidence (Vol. 215)', Princeton University Press, Chap 2

Hilton, M, McKay, J, Mouhot, JF & Crowson, N2013, 'The politics of expertise: How NGOs shaped modern Britain', Oxford University Press.

Marshall, A 2013, Principles of Economics, Palgrave Macmillan, Chap 1 &2

Ros, J2013, 'Rethinking economic development, growth, and institutions', business economics assignment Oxford University Press. Chap 1

Wang, HK2016, 'Energy markets in emerging economies: strategies for growth', Abington, Routledge.