Data Analysis Assignment: Reimagining The Bank Of Tomorrow

Question

Task:

Details:

Research reports must stick to the facts, and interpretation of facts. The aim of the research process itself – data collection and data analysis – is to establish the facts; subsequent analysis and discussion aim to contextualise the established the fact-base to the problem at hand. Research reports should also aim to not just regurgitate data but weave it into an overall narrative structure that is stimulating and valuable for the reader.

Only primary research is required. This data analysis assignmentevaluates your ability to conduct primary research (first-hand data collection) and does not require any secondary research.

Part 1: Interview (summary)

You are required to run an interview as per guidelines provided in class (you may do more than one if you wish). Instructions and guidelines on interview preparation and interview technique will be given in class, and you are expected to do some self-guided reading around this as well. This will help uncover higher-order motives beyond functional (evident) motives of the end user.

In this section of the report you are expected to write a short summary of the key interview findings, supported with illustrative quotes from your interview transcript. (The transcript itself belongs in the appendix, not the report body.)

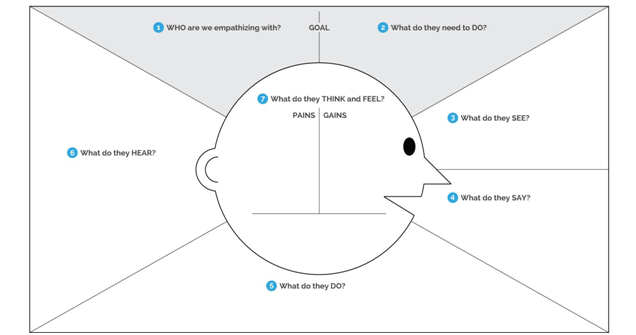

Part 2: Empathy map

After completing the interview section, organize your insights on an empathy map. Include this tool and some brief contextualizing commentary for the reader.

It must at least introduce the tool you're using and summarize the key takeaways for the reader. Part 3: Journey map

After completing the interview and empathy map sections, organize your findings on a journey map. Include this tool and some brief contextualizing commentary for the reader. It must at least introduce the tool you're using and summarize the key takeaways for the reader.

Part 4: Data analysis (summary of data/discussion of key themes)

Prioritize the top three to five themes appearing in your data – those likely to be most pertinent to the purpose of the research, as outlined by the assessment brief and/or your instructor. Then, conduct a brief discussion in the final section of the report (approx. 2 pages) of these key themes. Consider the following questions for elaboration:

What data points overlapped/re-enforced oneanother

What data points seemed to conflict with one another

If further research were being conducted, what would your recommendations be to the research team

How strong/conclusive was the evidence

Is it likely that other users may feel very different to that which is represented in this data set What key questions are still unanswered

Part 4: Data analysis(continued)

Although such analysis of limited scope may be seen as merely preliminary in the overall context of a design project/process, you should show the reader two key things in the Data analysis section:

a) that you uncovered a deep data set, and that you understand it

b) that you understand the research process well enough to know the limitations of your data, and what perspectives might still be missing

Part 5: Appendix (supporting evidence)

The appendix should contain any and all supporting evidence relevant to your primary research (and the audience for which the report is intended). Use the appendix wisely, and do not neglect it! At a minimum, this section should contain your interview transcript(s). Ideally, it should also include anonymized key demographic details of your interview participant(s) such as age, sex and user-type.

Answer

Part 1: Interview

Question 1: What is the purpose of the Commission's proposal for a framework for financial recovery and resolution

According to the first interviewee as portrayed within this data analysis assignment it is stated that during the financial crisis, certain large banks were deemed "too big to fail," and they were bailed out by the government using taxpayer money. The degree of help provided by the government was unprecedented. Despite the fact that this was essential in order to avert widespread market turbulence, it is evident that public monies should not be spent in this manner at the cost of other public objectives.

When it comes to the opinion of the second interviewee it is analysed that financial stability must be improved in the future in order for bailouts by the government to become less often required. There are severe inadequacies in the present mechanisms available to authorities to deal with bank failures, as shown by the well-known mortgage defaults that arose even during crisis. They also demonstrated that providing financial assistance to banks that are too large to fail but have limited financial resources is becoming more unsustainable. Artificial intelligence (AI) equipment is becoming more prevalent in our lives, with applications ranging from quick translation to voice recognition.

Based on the third interviewee it is emphasized that for the financial services industry, this is particularly true since disruptive AI-powered innovation is already being introduced to the market by competitors. Established banks must put artificial intelligence (AI) foremost in their ambition and implementation if they are to stay competitive. It consists of the possibly longer, AI-enabled planning and control, reference implementation, and specialized network growth strategy.

Question 2: What is the purpose of this framework

As analysed by the first interviewee it is examined that a transparent and thorough banking resolution framework is vital for ensuring long-term economic independence and reducing the potential public costs of a future credit collapse in the event of one. "Solution" refers to the reformation of an agency in order to preserve the continuance of its key functions, to safeguard economic independence, and to regain the survival of the organisation in its whole or in a portion of it.

According to the second interviewee it is analysed that the Crisis Management Framework offers a more comprehensive and effective plan to cope with bad loans at the federal level, as well as a mandatory orientation for responding with cross-border banking crises and therefore more people are agreeing on the terms of reimagining the bank of tomorrow. By acting as a powerful market enforcement component, effective settlement also solves the problem of adverse selection. In this way, resolutions are a vital supplement to other operations intended at improving the overall health of the financial system. Based on the third interviewee it is examined that capital adequacy levels and better financial composition, more fractional reserve protection, healthier and more accessible marketplace structures and practices, and improved monitoring are all ways to help banks become more resilient. The framework put up is a critical first step toward continuous improvement and cooperation in the Single market by guaranteeing that failing banks may be addressed in a manner that protects economic independence while reducing expenses to consumers and the general public.

Question 3: What would be the structure of financial assistance inside groups

As stated by first interviewee they obtain permission for firms within the group to sign into contracts with one another in order to assist other areas of the group (parent or subsidiary). Due to the fact that this provision operates in both ways, the parent business may provide help to the subsidiary, as well as the subsidiary providing support to the parent firm.

According to the next interviewee a request for such help must be authorised by the administrators of each subsidiary / parent organization, as well as the shareholder of each firm for which the aid is being requested. It must not have an adverse effect on the viability of the sponsoring business and must not result in a violation of minimum capital requirements in order to restore or ensure the sustainability of the whole Group.

As examined by third interviewee supporting a group may be advantageous to a subordinate since the whole group will be stronger and, as a result, will be better equipped to service the subsidiary's needs, for example. This, however, cannot be done at the expense of the subsidiary's goals and objectives. The Benefits of a New Approach to Customer Engagement: Better efficiency, higher trade agreements, and growing customer retention rates are just a few of the benefits of redesigning customer experience for banks.

Part 2: Empathy map

Think and feel: The feeling and thinking of 'Transforming product stories to design the virtual financial institution of future' that this concept was really grasped and demonstrated. The use of Big Data Technology at Bank began with recognition of the most important extrude in mindset that exists inside institutions. The competition does not consist of rival banks, but rather fin-tech companies that have been gaining traction into the monetary offers market. The most straightforward way for banks to become more relevant is to reimaging banking as something that is easy, frictionless, and undetectable (Kopiski and Wróblewski 2021). To get to that point, banks must be willing to re-architect their systems in order to be more psychological.

When it comes to the journey in the direction of technological metamorphosis, just as every mortgage lender has its own distinctive organisational route, there are others that choose a completely different path. A financial institution that makes a different decision will, as a result, go beyond customer platforms such as online applications or online payments, understanding that total digitization will emerge on the financial organization's next point.

Hear: In order for a firm to succeed, it must first understand its customers' preferences. Only then can it build effective consumer communications. This is truer now than ever before in the world of Covid. Banks, however, were already rethinking their knowledge of customer interaction before the epidemic, particularly when it came to product design, providing, marketing, and consumption. The international development crisis has made it quite evident that they are critical. Banks must find a means to either survive or get a competitive edge in order to thrive.

Say and Do:It is opined that Banks must generate long-term profitability if they are to maintain a competitive advantage and effectively in the long run. This is only achievable if you are able to completely reimaging the value individual deliver to their clients. Using the most up-to-date technology is no longer sufficient. Beyond that, everyone must give a distinctive and delightful customer experience to those that engage with them. This is most likely one of its most critical factors in determining a bank's long-term success (Ochoa, 2021). See:Banks have transitioned away from the notion of short-term projects and toward a platform model that incorporates long-term views as well as priority depending on the value of what needs to be constructed. In addition, everything was redesigned on a non-operational basis, and efforts were made to achieve complete digitization of the organisation. The most important step is to transition from projects to a device in order to take a long-term approach to product design (Thelusma, 2018). The second goal is the establishment of independence, self-organized, increased, dynamic cross-functional teams that are capable of working together. The final step is entirely automated. The principle is concerned with designing for contemporary systems. The step involves reorganizing the bank's concept such that management is stacking and technology is stacked with industry, so assuring that there is no firewall between the two key sectors. Gain:Technology plays a critical role in achieving this goal of allowing for customization across the financial industry. Banks must do more than merely digitize items / products; they must do more. To innovate various methods that may enhance the lives of their consumers outside of the sale of their main goods, it is necessary for them to reevaluate their understanding and reimagining their thinking.

Organizational culture has an important supporting role in this endeavour, and companies that foster a spirit of knowledge continue to develop more effectively and quickly as a result. The quantity of data accessible to banks allows you to experiment and see what banks provide their consumers and how they build their products and services. The data will also enable banks who want to be client-centric with the adaptability they need in order to respond to rapidly changing surroundings and consumer expectations.

Pain: The bank's servers will be inaccessible if they are unavailable or unexpectedly unreachable due to scheduled system maintenance, which will prevent them from accessing their bank data online or on their mobile device. In the vast majority of circumstances, they can do your ordinary financial institutions on their own time. But it might be harder to resolve an issue if users do not have a deep connection with their lender when it occurs.

Part 3: Journey map

|

Awareness |

Interest |

Evaluation |

Decision |

|

Financial institutions of all sizes were in catastrophe mode during the early stages of the corona virus disaster, adjusting to the sudden change to virtual banking as consumers were unable to access shuttered branches or were hesitant to visit the ones that were still open due to the virus' spread. Improving on-line and cellular financial capabilities is just the tip of the iceberg, as most banks and credit score institutions re-evaluate their whole information technology infrastructure in light of COVID-19 (Das et al., 2018). After years of relative complacency, financial institutions are really being pushed out of established comfort zones, with the recognition that advanced technology must be integrated across the organization in order to achieve overall performance objectives in the future. The majority of financial institutions are aware of the advantages of the modern period as a source of inspiration for technological reinvention. Nevertheless, for a myriad of purposes, the majority of businesses have only hesitantly embarked on this journey up till now moment.

|

People have taken a significant stride forward in repositioning itself as a generation organisation with a license to conduct a financial provider enterprise (Olufadewa et al., 2020). It is the application of era to include its presence into the routine excursions of consumers. Whether that was a search for better health, better transportation, or maybe better entertainment, Ping An offers a framework organization and environment interactions (and, of course, a covered offering!) to make the trip more convenient. For example, if a banking institution is currently assisting a customer's home purchase via collaborations, it may prompt more excursions with recommendations for prosecution companies, movers and packers, application firms, and interior designers at the precise moment they are required. |

Redesigning the Consumer Experience is not even a one-time exercise. It demands ongoing creativity and several revisions. If people have contradictory ideas, this is a wise to check them in succession (using A / B testing, etc.) before settling on one(OLALERE et al., 2021). With the shift to openness financing, universal banks (banks that produce, own and buy products and services via their own channels) will use a platform business model to acquire a range of financial and non-financial products through the following networks: became. Combine and disperse companions from communities that may assist grow. Banks need to engage with their partners to develop and grow their services and leverage these interconnections to enhance, empower and enhance their customers' experiences to meet this tendency. Banks must repay such thinking by engaging in these bigger journeys by being there right from the moment the consumer acts on a fundamental need. |

Purchasing a portion or all of a technology company is becoming a revolutionary step for the largest and most powerful corporations and organisations. It is seen as a comparative advantage in the fields of payments, artificial intelligence, and digital skills. A big National bank has bought a significant artificial intelligence startup in order to broaden its approach. Some Eastern banks employ more than 10,000 engineers who are focused on artificial intelligence and cutting-edge technologies (YuSheng and Ibrahim 2020). Existing employees are shifting from innovation laboratories to personal leadership of outcomes, putting them at more risk when it comes to launching innovative digital services. In order to motivate and inspire innovators to risk banks to become digital leaders, investment teams or human resource partnerships are used. It takes happening at AI centres and colleges all around the globe as part of this talent search. In the hyper-digital age, it is evident that conventional banks will be replaced by a technological business that will compete for customers. The expansion of tech-fin will benefit established businesses, and challenger banks will attempt to drive their clients toward innovation. |

|

Insights and new ideas for innovation |

|||

|

Researchers have long been interested in the link between consumer happiness and business success. Their findings demonstrate a direct association between excellent customer service and commercial success. Recent research by the Institute of Dealing With customers shows that enterprises with above-average customer satisfaction increase yearly revenue by 9.1%, while those with below-average service quality important business by 0.4%. Only growth has been achieved. Retention department, engagement, and merge outcomes drive positive revenue growth. With the proper customer experience, current customers may become advocates who help increase new customer acquisition rates. Clearly, happy customers = happy business (Gruin and Knaack 2020). And IT and industry leaders know it. In business and technology circles, improving CX has been shown to improve consumer acquisition, employment, revenue, and cost-to-serve KPIs. However, many executives appear to lose focus something between “recognizing the importance” and “taking action”. In payment institutions, top executives acknowledge a desire to enhance customer experience, but few appear to have developed a clear strategy or show the energy required to drive change. |

|||

Part 4: Data analysis

Theme: purpose of commission’s proposal for a framework for financial recovery and resolution.

According to the theme the interviewee had different perspective and according first interviewee “The government's assistance was unmatched in its scope and generosity. No matter how important it was to avoid broadly diversified instability, it was still a mistake.” Based on this particular statement it is analysed that banks may determine which visits are most important to them depending on their individual circumstances. An in-depth awareness of these facts, on the other hand, is the first step toward a successful customer experience conversion. Implementing proper prioritizing matrixes and making relevant organisational adjustments to support speedy execution are required for converting these insights into actions (Martin-Sardesai and Guthrie 2019). "In order to lessen the frequency with which government bailouts are required in the future, we must strengthen fiscal stability," stated the second responder. True customer centricity, on the other hand, demands that everyone in your business understands how they may contribute to achieving favorable customer outcomes within the confines of their respective roles and responsibilities.

Next interviewee thinks that frameworkput up is a critical first step toward continuous improvement and accordingly the definition of a customer-centric company is one that is always focused on learning and growth across the business in order to satisfy fast changing consumer expectations. Finally, identifying the appropriate yardstick and monitoring performance on a regular basis serves as a baseline and a motivation for driving continuous improvement efforts.

Theme: purpose of this framework

As per the first interviewee, it is analysed that “protecting long-term economic self - sufficiency and minimizing the possible public costs of a future financial crisis, should one occur” and based on this Business and organisational transformation is not about how intelligent, agile, and productive creativity machines and organizations are; rather, it is about how accurately and thoroughly individuals inside an organisation comprehend what change means at the interpersonal level and apply that understanding (Ransdell, 2019). According to second intervieweeacting as a powerful market enforcement component also it helps in adding value to the company's bottom line. Each function, duty, and range of power has an impact on the other. Emphasizing particular above others may be beneficial to financial institutions. Many banks today seem to be implementing effective procedures that synchronize and support multidisciplinary efforts to rethink the customer experiences of selected consumers, which is a good thing. Based on third interviewee “better financial composition, more fractional reserve protection, healthier and more accessible marketplace structures and practices”therefore the customer journey is being prioritized in the restructure of client service groups at big banks, rather than the traditional different units of human resources.

Theme:structure of financial assistance inside groups

As stated by first interviewee they are ensuring that banks need to become far more customer-centric than they ever have been. Based on second interviewee it is analysed that rather than talking to customers using industry jargon and product names, they need to put their customers in the driver’s seat so that they can access information. As examined by third interviewee it is found that AI as of today works well only if narrow, so they need to look at players who are focused on specific domains or else quality and low level of business (Li et al., 2018).

References

Das, P., Verburg, R., Verbraeck, A. and Bonebakker, L., 2018. Barriers to innovation within large financial services firms: An in-depth study into disruptive and radical innovation projects at a bank. European Journal of Innovation Management.

Gruin, J. and Knaack, P., 2020. Not just another shadow bank: Chinese authoritarian capitalism and the ‘developmental’promise of digital financial innovation. New political economy, 25(3), pp.370-387.

Kopiski, D. and Wróblewski, M., 2021. Reimagining the World Bank: Global Public Goods in an Age of Crisis. World Affairs, 184(2), pp.151-175.

Li, Z., Liao, G., Wang, Z. and Huang, Z., 2018. Green loan and subsidy for promoting clean production innovation. Journal of Cleaner Production, 187, pp.421-431.

Martin-Sardesai, A. and Guthrie, J., 2019. Social report innovation: evidence from a major Italian bank 2007-2012. Meditari Accountancy Research.

Ochoa, A., 2021. Filling the Gaps: Reimagining Public Space as a Continuum (Doctoral dissertation, Carleton University).

OLALERE, O.E., KES, M.S., ISLAM, M.A. and RAHMAN, S., 2021. The Effect of Financial Innovation and Bank Competition on Firm Value: A Comparative Study of Malaysian and Nigerian Banks. Data analysis assignmentThe Journal of Asian Finance, Economics and Business, 8(6), pp.245-253.

Olufadewa, I.I., Adesina, M.A. and Ayorinde, T., 2020. From Africa to the World: Reimagining Africa’s research capacity and culture in the global knowledge economy. Journal of Global Health, 10(1).

Ransdell, J., 2019. Institutional innovation by the Asian infrastructure investment bank. Asian Journal of International Law, 9(1), pp.125-152.

Thelusma, M., 2018. DWELLING, COMMUNITY, AND RESILIENCE: Reimagining Tomorrow in Port-Au-Prince (Doctoral dissertation).

YuSheng, K. and Ibrahim, M., 2020. Innovation capabilities, innovation types, and firm performance: evidence from the banking sector of Ghana. SAGE Open, 10(2), p.2158244020920892.

Appendix

Interviewer: What is the purpose of the Commission's proposal for a framework for financial recovery and resolution

Interviewee 1: I think that the main purpose of proposing the framework of financial recovery and resolution is to avert the widespread marketplace turbulence. This makes the public objectives more subtle.

Interviewee 2: In my opinion the financial stability matters the most for this specific purpose and to identify the severe inadequacies.

Interviewee 3: I beg to differ from both the interviewee because in my perspective AI powered could be major purpose in order to be competitive.

Interviewer: What is the purpose of this framework

Interviewee 1: In order to maintain long socioeconomic stability and reduce the possible public costs of a subsequent financial meltdown, a comprehensive financial resolution structure is essential in my perspective.

Interviewee 2: As per my understanding successful resolution overcomes the issue of information asymmetry because it acts as a healthy economic compliance feature.

Interviewee 3: I think that by ensuring that failed banks may be dealt with in a way that maintains economic stability, the mechanism formulated and implemented is an important first step forward continued progress and collaboration in the Free Trade area.

Interviewer: What would be the structure of financial assistance inside groups

Interviewee 1: As per my examination and understanding it is more relevant if likewise, the parental business will offer assistance to the branch, and the conglomerate may provide some assistance to the holding company.

Interviewee 2: As a worker in a bank it is stated that they never have a negative impact on the profitability or viability of the corporate or private and must not put them in breach of regulatory capital requirements.

Interviewee 3: I think that it will give the benefit to the customers regarding their engagement and retention when it comes to the workers.