Finance Assignment: A Detailed Analysis On Future Safe Investment Product

Question

Finance Assignment Task:

You have just read a press release from a major competitor announcing the Allianz Retire+ Future Safe structured investment product. Details of the product can be found at https://www.allianzretireplus.com.au.

You are required to advise your Management Committee on this new product. Specifically, the Management Committee would like you to:

- Provide an overview of the structured investment product environment.

- Provide a detailed analysis of Allianz Retire+ Future Safe structured investment product and the parties involved in developing this product.

- Explain in detail how your firm may be able to create (i.e., manufacture, replicate) essentially the same product as the Allianz Retire+ Future Safe structured investment product using combinations of other financial instruments.

- Provide a detailed analysis of the market risks your firm would face in offering such a product and how your firm may be able to hedge those risks.

The Management Committee requires your advice in the form of a report that contains an executive summary, body, recommendations, conclusions, and references.

Answer

Executive Summary

As seen in the present scenario of finance assignment, the investors have to deal with some uncertainties, while facing various risks associated with them. Therefore, in such uncertainty, a structured investment product can be an attractive tool for investors. In general product investment structure is the types of investment that are designed to meet the requirement of the investors, along with the customized mixed product. It generally includes the usage of derivatives, and they are often formed by the investment banks in order to hedge funds, client mass market, and the organizations. Within this context, Allianz Retire+, renowned life insurance limited of Australia, offers a wide range of future Safe structured investment products, while ensuring growth security, income, and flexibility to the investors. It has been identified that the Allianz Retire+ offers various levels of protection to the investors while protecting their investment in the downturn of the share market. In concern to create the same future Safe structured investment product offered by Allianz Retire+, this report has analyzed the usage of financial instruments in order to replicate the product. The report culminates with the analysis of market risk associated with it while suggesting some recommendations to the management of the firm in order to overcome the identified risk.

Introduction

Retirees need unique plans and strategies to earn after retirement and live their life without any hindrances. Allianz Retire+ is a company that provides retirees with various facilities to be availed to keep earning money even after they stop working. Allianz Retire+ is a company based in Australia and has allied with the PIMCO to deliver high standard financial stability and security during and after retirement. Allianz Retire+ has launched a product known as future safe which provides a range of facilities to retirees. Future safe has been developed for retirees and investors who do not want that their lifetime savings come at risk after investment. Future safe protects the investments from downturns in the market and helps in generating incomes along with supple withdrawal choices. Exposure to market-related investment is provided by Future Safe and it allows the investors to reallocate each year.

This report sheds light on the overview of the environment of the investment product, which is Future Safe. A detailed analysis has been provided of the Future Safe investment product and the involvement of the parties in developing the product has also been discussed. The methods, by which the firm will manufacture or reproduce the same product as Future Safe of Allianz Retire+, have been talked about elaborately in this report. The combined usage of financial instruments to develop the product has been discussed for the given company. There is a range of market risks involved in offering the aforementioned product (D’ALPAOS and CANESI, 2014). The company which is developing the same product as Future Safe may face market risks also; the market risks of the company have been identified, discussed and evaluated in the report to provide the company with the required solutions. Appropriate advice has been provided to the management committee of the firm to help them create a similar product without facing many market risks.

1. Overview of the structured investment product environment

The environment of an investment product covers several subjects. The success or failure of the investment product depends on its surrounding environment. The environment must be closely analysed before the development of any investment product to ensure the success of the product. The following factors must be considered before developing an investment product:

- Investments and assets medium- The firm should choose from the variety of assets that exist in the market. The assets include corporate bonds, real estate, share markets, municipal bonds, government bonds and many more. The management of the company must choose from the aforementioned types of assets to decide regarding which asset the investment product has to be developed.

- Financial markets- Financial markets are where the asset sellers and buyers deal with each other. One of the major features of these markets is that the forces of this market determine the asset price (Madura, 2020). The characteristic of the financial market is stock market, foreign exchange, cash markets and many more. It is crucial for the company to evaluate this market before the development of the investment product.

- Structure of the market- The stock market is the most widely followed market around the world. The structure of the market includes the features of the financial market along with mortgage, equity, foreign exchange, debt and derivatives market (Farboodi, Jarosch and Shimer, 2017). The firm can focus on the stock market and debt market for the development of its product as these two markets observe most of the investments. The firm should also analyse the market competition for effective product development (Alimov, 2014).

- Intermediaries of the market- This area includes the consideration of the factors like insurance companies, pension companies, commercial banks, financial advisors, stock exchanges, investment banks and many more. The intermediaries play a vital role in the investment process and it affects the investment decisions of the investors, thus, it is important for the investment product development company to consider this area before developing plans and strategies for their product development.

- Investment process- the steps required in creating an investment and asset portfolio falls under this process (Ilin, Koposov and Levina, 2014). This is analysed based on the interests and investment policies of investors and companies which develop investment products must analyse this process critically to gain deeper knowledge about the choices and preferences of the investors. This process covers the subjects about the diversification of the investments of investors. The investments strategies are developed based on the analysis of this market.

- Regulation- One of the major aspects of the investment environment is, the regulation of securities markets. The financial market trading is regulated by surplus laws and it is ensured that adequate information is provided to the investors and traders so that they could make appropriate decisions related to investments. The regulation of the financial markets also prevents fraudulent activities and allows investors to access authentic information to make their investment decisions. It is important for the firm to critically analyse the regulations of the financial market before they start the development of the product so that they can easily make decisions on the areas that would require emphasis.

- Economy- The prices of the assets are affected by several factors which include monetary policies, GDP, fiscal deficit, inflation and many more. The most important decision in the domain of asset management is the allocation is assets and any company which develops investment product must contain deeper knowledge about the economic conditions and factors which affects the investment domain. Both the global and domestic economic conditions are analysed to make decisions regarding the allocation of assets and investments.

2. Detailed analysis of Allianz Retire+ Future Safe structured investment product

Allianz Retire+ is an insurance company and is well known for the services and security they provide to their customers. In Australia, most of the older people are living longer and they do not have any money security where they could keep safe their money and get expected returns after retirement to enjoy their life. As of the report of 2017, around 3.8 million of Australia’s population is 65 plus aged people and that is around 15% of the total population of the country. This also means that the people are living longer with their healthy life. However, after retirement, they need to sustain and live their life and they do not get any sufficient amount of returns from their saved or invested money (Allianz Australia Life Insurance Limited, 2019). The Allianz Retire+ has come up with new innovative ideas to bring light to the life of the retirees for a good and secure living after retirement. Allianz Retire+ future safe was the product that was designed from the perspective of the customers and not from any kind of business earning purposes. The company did market research and found that most of the retirees of Australian people are facing various financial challenges after retirement. The research was done by the Allianz Retire+ also highlighted that most of the non-retirees of Australia think that they will not have enough money to live their life comfortably after the retirement and this brings concern to their retirement planning about money and lack of security, confidence and protection to live (Allianz Australia Life Insurance Limited, 2019).

Allianz Retire+, a part of the Allianz group offers a wide range of insurance services both for personal and corporate, which includes life and health insurance, property, assistance services, global business and credit insurance. With the efficient services, the company has more than 100 million customers, along with 147,000 employees, insuring approx 3.5 million Australians. The Future Safe structured investment product of Allianz Retire+ is specially designed for retirees and investors who intends to avoid risking their savings. It is an investment product that protects one's investment from market downturns while generating income and offering flexible options. It provides security, growth, income and flexibility to investors while protecting their investments (Allianzretireplus.com, 2021).In Future Safe of Allianz Retire+, the investment product is well structured to understand the safety and security of the retiree’s money. The investment plans provide access to investment from the year 20 to retirement date where they have to pay a tax rate of less than 30% unlike in the other share market and also provides a guarantee of money returns.

Fig. 1- Aspects of Allianz Retire+

Source- (Allianzretireplus.com, 2021)

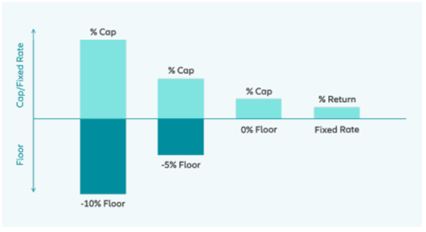

The Future Safe structured investment product of Allianz Retire+ provides access to share market-linked returns in a simple way, along with higher certainty. It helps in terms of protecting the retirement saving when there is a downturn in the share market because it is an investment product that is issued by the life insurance company. The protection option provided by the Allianz Retire+ future Safe structured investment product offers three levels of protection, along with one year fixed rate, depending upon the level of loss that the investors are comfortable with.

Fig. 2- Protection option offered by Allianz Retire+

Source- (Allianzretireplus. com, 2021)

The maximum, loss suffered by the investor depends upon the floor they choose, where each floor has a Cap linked with it, which is the maximum gain in a year. Therefore, the lower the floor, the higher the Cap will be. This also brings flexibility to choose their floor and invest the amount and gets assured and expected returns. In the Future Safe investment product, various investment plans are also available for the retirees or to the customers that help them to invest as per their choices. The investment options are as follows, S&P/ASX 200 Total Return, S&P/ASX 200 Price Return, MCSI World Net in Australian Dollar and Fixed Rate. The retirees can choose any of these options and can invest the money for safe returns. This also brings flexibility to the customers that they could change the options yearly at the anniversary date of the investment. The investment plan is for the interval of 7 to 10 years and can withdrawal the amount or can invest it further to the other investment plans. The Future Safe investment plans also provide flexibility to the customers as they can take advice from the financial advisors in the first year of the investment which will be the best for them and can get the best financial returns (Allianz Australia Life Insurance Limited, 2021).

The investment options of Allianz Retire+ Future Safe investment plans give the best options for their customers so they do not have to worry about market loss and security. The policyholder also can nominate the beneficiaries if death occurs in times of invested years. The investment options also help to know that the retirees or the customers do not have to bear any loss on investing the amount and even if the share market faces any kind of market loss. The minimum the retirees needs to invest in the investment plan for 7 years or 10 years is $20,000 and the maximum of up to $1.6 million and $5 million (allianzretireplus.com, 2021).

The parties involved in developing the Future Safe product are the board team members of the Allianz Retire+ and the other investors that include the share market holders and the retirees that helps to bring this investment plan business to success and sustain in the competitive market edge (allianzretireplus.com, 2021). The researcher of the Allianz Retire+ is also the significant party that helped to do the deep market research and to analyze the needs of the market.

3. Analysis of financial instruments to create a structural product

Financial instruments are said to be the assets that can be sold, or they could also be seen as a capital package, which might be dealt with. Hence, most forms of financial instruments deliver effective transfer and flow of capital all during the financiers of the world(Paduszy ska, 2020). These assets could be cash, a contractual right to offer or get cash or another form of financial instrument, or verification of an individual's rights of an entity. In simple terms, financial instruments could be valid or virtual records representing a lawful agreement including any form of financial value. However, in order to create a structural product the same as the Allianz Retire+ Future Safe structured investment product, Cash Instruments and Derivative Instruments have been taken into considerations.

Cash Instruments- Financial instruments are intangible assets that are anticipated to deliver future benefits which will eventually help to secure the future of an individual with the form of a claim to future cash. The product of Allianz Retire+ Future Safe mostly focuses on clients who want to secure their future after retirement. Hence, this insurance investment firm helps them to provide a tradable asset through legal contractual right to verify monetary value or the entity's ownership interest(Ivan et al., 2015). Here, it can be said that the ideals of cash instruments are determined and influenced openly by the markets, which generally means that the client will be attracted by the services wherein they consider that securities are easily exchangeable. There are two forms of cash instruments and they are deposits and loans and, and loans. Both loans and deposits are measured as cash instruments as they symbolize financial assets that have several forms of contractual affiliation between both the parties i.e., the insurer and the clients.

Derivative Instruments- This financial instrument has ideals derived from underlying assets, such as a bond, resource, stocks, resources, and stock indexes. The derivative instrument is valuable for insurance firms that would like to hedge their experience to ruinous losses. Hence, these instruments commit to delivering fundamental products at a certain time in future or deliver the right to sell or buy them in the future(CFI, 2015). Considering this financial instrument, the insurance firm will help to offer beneficial products and services to its clients for future use. However, derivative instruments have different forms and they are:

Forward agreement- It delivers the owner the liability to sell or buy a certain fundamental instrument at a particular date in the future at a specified rate.

Swaps- This is said to be the agreement wherein both the parties have the same opinion to exchange cyclic payments. The amount of cash for the exchanged payments is based on a certain determined value amount(Simpli, 2012).

Future agreement- It is the contract between the parties wherein both the parties need to agree to exchange the payments in a cyclic method. The amount of cash for the exchanged payments is based on a certain determined value amount.

Options- It is the agreement wherein the option insurer allows the option client the right to go into the transaction with the prior insurer to either sell or buy a fundamental asses tar a particular rate on or prior to a particular set date.

Moreover, with two selected combinations of financial instruments, the product will be more beneficial or valuable for the firm to attract more clients and to secure their future after retirement. Furthermore, it can be said that adding these financial instruments can strengthen the features of the product but adding an alternate option for payoff will eventually help to boost the service of an insurance firm. The payoff will help to make the client understand the profit they are about to get by enrolling on the future protection plan (week 3). Hence, a payoff diagram has been shown below to create a convenient way to envision what occurs with the strategies of option as the underlying asset value changes are with the practice of the payoff diagram.

Fig- Diagram of Payoff

Source-(Nissim, 2010)

However, considering the derivative instrument, the payoff of a forward contract is its price at maturity of the insurance policy.

For instance, F0, T= agreed of the forward rate at t=0, to be received or reimbursed at expiration t =T

ST= Expiration of underlying value asset

Concerning this, the outcomes might be portrayed at any point in time, though the graph in the diagram generally shows the outcome at the expiration of the options included in the strategy for a better financial insurance plan for the clients. Within the above diagram, the vertical axis emphasizes the profits or losses in the date of options expiration ensuing from a specific strategy, when the horizontal axis focuses on the fundamental price of an asset on the date and day of the options expiration. In addition to this, the forward buyer focuses on the long term underlying asset, on the other hand, the seller focuses on the short term underlying asset and it generally reflects the profit and loss through the payoff diagram.

4. Detailed analysis of the market risk

The investment-related risk is of two types-systematic and unsystematic risks and the systematic risks are known as market risk. The market risks mainly include debt risk, foreign exchange risk, commodity risk, and currency risk. The product developed for our firm is similar to the Future safe investment product of Allianz Retire, and it contains options to invest in both domestic as well as global market. In the case of the Global equity investment option, the foreign exchange-related risk and currency risk are the prime market risks that may be faced by investors. The foreign exchange risk may occur during the international financial transaction because of currency fluctuations. As the product of the firm will deal with the foreign market too, the investors who will choose the investment option in the global equity market will be mainly exposed to the risk. The domestic equity investment option carries the risk of currency that may occur due to a financial crisis in the country or an economic recession that heavily shook the price movement. The market risk related to the new product of the firm is also based on the willingness of investors to bear the risk (Mathews, 2019). The investment portfolio can be developed with the combination of investment options that simultaneously diversify the risk for the investors through different investment options, or an investor can select the high-risk-based investment options aiming to gain better returns. The diversification of risk in the investment portfolio is another factor that causes risk differences among investors.

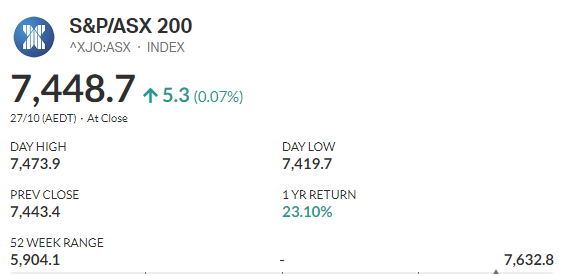

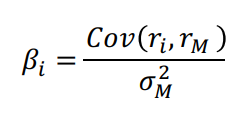

The calculation of risk is a crucial part of the investment for the new product that will make the investors able to understand the risk, the factors related to risk, and the amount of risk that have to carry with a specific investment option. The systematic risk or the market risk is measured with the help of the beta coefficient that helps to estimate the sensitivity of the market portfolio return. Measuring the performance of the listed companies and the historical data on their performances also makes the investor able to estimate the risk for the future specifically for the short-term. S&P/ASX200 is the share market index of Australia that is designed to measure the historical performance of 200 listed companies (Market index, 2014).

Source:(Market index, 2014)

Another way to measure the systematic or market risk is a calculation of beta coefficient using the formula shown in the picture below:

Based on the results of the beta coefficient, it can be said how much an investment option carries the risk. If the result of beta is equal to 1 then the systematic risk is similar to market portfolio risk, if the beta result is greater than 1 then the systematic risk is more than the market portfolio risk, and lastly, in the case of a small amount of beta than 1, the systematic risk is less than the market portfolio risk (Gardner, McGowan and Moeller, 2010).

Recommendations to mitigate the risk

It is important for the firm to develop risk management strategies to minimize the risk related to the product. The ways the risk can be hedged are the following:

- Selling forward: it is a profit hedging option, in which the firm will lock a specific price for their product and sell the product to the customers at the fixed price specified for the product on the specific duration. The selling forward option will allow the firm to eliminate any kind of uncertainty regarding the price of the product and will be able to earn a specific amount of profit. The key benefit of the selling forward strategy is the firm will be able to earn a certain amount of profits

- The proper use of risk calculation: The risk calculation related to investment options not only ensures risk mitigation of investors but also increases the reliability of investors more on the firm. The capital asset pricing model should be used to calculate the risk and to anticipate the return on the investment. The key advantage of using CAPM to calculate risk is to reflect on the exact relationship between the systematic risk and required return (ACCA, 2020). Compared to the dividend growth model, it is more effective to calculate the risk as it considers both the systematic risk based on market scenario and company level.

- Buying a put option: It is another strategy to reduce the market risk for the firm and to ensure good profits. It will allow the firm to gain higher profits based on the floor price. It will be beneficial for the firm based on the price movements; the firm can leave or accept the guaranteed price (Smith and Anderson, 2020). In the case of, market fluctuations, the firm has the option that will give price protection at the selected strike price.

Conclusion

After the overall analysis of the report, it has been identified that it is crucial to analyze the environment of investment product, before making any developments, because both the success and the failure greatly depends upon its environment as well. In order to develop an investment product, it is essential to consider certain factors such as investments and assets medium, finance, and structure of the market, and the process of investment. In concern to the development of product investment, it has been noted that the Future Safe structured investment product offered by Allianz Retire+ is at optimum growth, with the influence of over 100 million customers in Australia. Considering the success of Allianz Retire+, the attempt has been made to replicate the similar product as offered by Allianz Retire+. In order to create the same product, the combinations of various financial instruments have been analyzed. Financial instruments are generally assets or capital packages that can be sold or dealt with while making a lawful agreement. However, the financial instrument that has been used both for the replication and enhancement of the product offered by the firm are cash instrument and derivative. These instruments are mainly used because they will not only in the replication of the Allianz Retire+ product, but it will enhance the product as well.

There are certain risks associated with the creation of a similar product as Allianz Retire. The risks that have been identified are mainly the currency risk and the foreign exchange risk. With this identified risk there are probabilities that the value of the investment may decrease because of the change in the relative value of the currencies that are involved. However, the identified risks can be overcome effectively by the use of risk calculation and selling forward financial instruments.

References

ACCA (2020). CAPM: theory, advantages, and disadvantages | F9 Financial Management | ACCA Qualification | Students | ACCA Global. [online] www.accaglobal.com. Available at: https://www.accaglobal.com/uk/en/student/exam-support-resources/fundamentals-exams-study-resources/f9/technical-articles/CAPM-theory.html.

Alimov, A. (2014). Product market competition and the value of corporate cash: Evidence from trade liberalization. Journal of Corporate Finance, 25, pp.122–139.

Allianz Australia Life Insurance Limited (2019). Allianz Retire+ launches first product | Media | Allianz Retire+. [online] www.allianzretireplus.com.au. Available at: https://www.allianzretireplus.com.au/about-us/media-room/media/allianz-retireplus-launches-first-product.html [Accessed 27 Oct. 2021]. Allianz Australia Life Insurance Limited (2021). Delivering retirement income solutions | Allianz Retire+. [online] www.allianzretireplus.com.au. Available at: https://www.allianzretireplus.com.au/institutional/retirement-income-solutions.html [Accessed 27 Oct. 2021]. Allianzretireplus. com (2021). Future Safe Features | Retirement Savings Protection | Allianz Retire+. [online] www.allianzretireplus.com.au. Available at: https://www.allianzretireplus.com.au/future-safe/features.html [Accessed 27 Oct. 2021].

Allianzretireplus.com (2021). Future Safe Overview. [online] www.allianzretireplus.com.au. Available at: https://www.allianzretireplus.com.au/future-safe/overview.html [Accessed 27 Oct. 2021]. allianzretireplus.com (2021). Future Safe Product Disclosure Statement. Future Safe Product Disclosure Statement. [online] Available at: https://www.allianzretireplus.com.au/ [Accessed 27 Oct. 2021].

CFI (2015). Financial Instrument - Overview, Types, Asset Classes. [online] Corporate Finance Institute. Available at: https://corporatefinanceinstitute.com/resources/knowledge/trading-investing/financial-instrument/ [Accessed 27 Oct. 2021].

D’ALPAOS, C. and CANESI, R. (2014). Risks Assessment in Real Estate Investments in Times of Global Crisis. [online] ResearchGate. Available at: https://www.researchgate.net/profile/Rubina-Canesi/publication/286462060_Risks_assessment_in_real_estate_investments_in_times_of_global_ crisis/links/56b99edf08ae9d9ac67e16df/Risks-assessment-in-real-estate-investments-in-times-of- global-crisis.pdf [Accessed 27 Oct. 2021]. Farboodi, M., Jarosch, G. and Shimer, R. (2017). NBER WORKING PAPER SERIES THE EMERGENCE OF MARKET STRUCTURE. [online] Available at: https://www.nber.org/system/files/working_papers/w23234/w23234.pdf [Accessed 27 Oct. 2021]. Gardner, J.C., McGowan Jr, C.B. and Moeller, S.E. (2010). Calculating The Beta Coefficient And Required Rate Of Return For Coca-Cola. Finance assignmentJournal of Business Case Studies (JBCS), [online] 6(6). Available at: https://core.ac.uk/download/pdf/268109757.pdf [Accessed 18 Sep. 2019].

Ilin, I., Koposov, V. and Levina, A. (2014). Model of asset portfolio improvement in structured investment products. Life Science Journal, [online] 11(11). Available at: http://www.lifesciencesite.com/lsj/life1111/038_25696life111114_265_269.pdf [Accessed 27 Oct. 2021].

Ivan, P., Dušan, C. and Tatjana, P. (2015). Role of Insurance Companies in Financial Market. [online] Available at: https://scindeks-clanci.ceon.rs/data/pdf/2217-9739/2015/2217-97391502094P.pdf [Accessed 27 Oct. 2021]. Madura, J. (2020). Financial Markets & Institutions. [online] Google Books. Cengage Learning. Available at: https://books.google.co.in/bookshl=en&lr=&id=a3TLDwAAQBAJ&oi=fnd&pg=PP1&dq=what+are+financial +markets&ots=nL9r-1I62k&sig=IIs0PbrGLZdb27pJXj6uIZZmZiY#v=onepage&q=what% 20are%20financial%20markets&f=false [Accessed 27 Oct. 2021]. Market index. (2014). S&P/ASX 200 - Shares Prices & Charts. [online] Market Index. Available at: https://www.marketindex.com.au/asx200.

Mathews, T. (2019). The Australian Equity Market over the Past Century | Bulletin – June Quarter 2019. Bulletin, [online] (June). Available at: https://www.rba.gov.au/publications/bulletin/2019/jun/the-australian-equity-market-over-the-past-century.html.

Nissim, D. (2010). Analysis and Valuation of Insurance Companies Industry Study Number Two. [online] Available at: http://www.columbia.edu/~dn75/Analysis%20and%20Valuation%20of%20Insurance%20Companies%20-%20Final.pdf [Accessed 27 Oct. 2021].

Paduszy ska, M. (2020). The Essence and Significance of Financial Instruments for Enterprises in Poland in 2010-2018. Finanse i PrawoFinansowe, 3(27), pp.109–124.

Simpli, L. (2012). Significance of Financial Instruments in Capital Management. [online] Simplilearn.com. Available at: https://www.simplilearn.com/financial-instruments-rar18-article [Accessed 27 Oct. 2021].

Smith, J. and Anderson, C. (2020). Kansas State University Agricultural Experiment Station and Cooperative Extension Service Risk Management Price Risk Hedging With a Put Option. [online] Available at: https://www.agmanager.info/sites/default/files/Hedging%2520with%2520a%2520put%2520option.pdf.