Finance Assignment: Financial Analysis For Businesses

Question

Task:

The questions to be answered within this finance assignment are:

Week 6

Cotton On Ltd. currently has the following capital structure:

Debt: $3,500,000 par value of outstanding bond that pays annually 10% coupon rate with an annual before-tax yield to maturity of 12%. The bond issue has face value of $1,000 and will mature in 20 years.

Ordinary shares: $5,500,000 book value of outstanding ordinary shares. Nominal value of each share is $100. The firm plan just paid a $8.50 dividend per share. The firm is maintaining 4% annual growth rate in dividends, which is expected to continue indefinitely.

Preferred shares: 45,000 outstanding preferred shares with face value of $100, paying fixed dividend rate of 12%. The firm's marginal tax rate is 30%.

Required:

a) Calculate the current price of the corporate bond?

b) Calculate the current price of the ordinary share if the average return of the shares in the same industry is 9%?

c) Calculate the current price of the preferred share if the average return of the shares in the same industry is 10%

Week 7

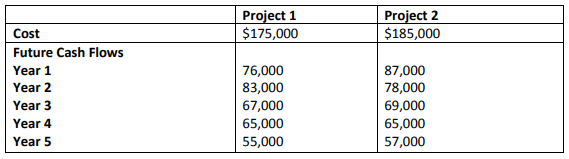

Giant Machinery Ltd is considering to invest in one of the two following Projects to buy a new equipment. Each project will last 5 years and have no salvage value at the end. The company’s required rate of return for all investment projects is 9%. The cash flows of the projects are provided below.

Required:

a) Identify which project should the company accept based on NPV method. (Note: Please round up the result of each calculation of PV to 2 decimal places only for simplification)

b) Identify which project should the company accept based on simple pay back method if the payback criteria is maximum 2 years.

c) Which project Giant Machinery should choose if two methods are in conflict.

Week 8

Bermuda Cruises issues only common stocks and coupon bonds. The firm has a debt-equity ratio of 0.45. The cost of equity is 17.6 percent.

Required:

What is the pre-tax cost of the company debt if weighted average costs of the company is 13.5% and the firm's tax rate is 35 percent?

Week 9

Western Electric has 35,000 ordinary shares outstanding at a price per share of $47 and a rate of return of 13.5%. The firm has 5,000 preference shares paying 7% dividend outstanding at a price of $58 a share. The preferred share has a par value of $100. The outstanding bond has a total face value of $450,000 and currently sells for 102% of face. The pre-tax yield-to-maturity on the bond is 8.49%.

Required:

a) Calculate the total market value of the firm.

b) Calculate the capital structure of the firm. (Please round up the result at 3 decimal places)

c) Calculate the firm's weighted average cost of capital if the tax rate is 30%, assuming a classical tax system.

Week 10

The Giant Machinery has the current capital structure of 65% equity and 35% debt. Its net income in the current year is $250,000. The company is planning to launch a project that will requires an investment of $175,000 next year. Currently the share of Giant machinery is $25/share.

Required:

a) How much dividend Giant Machinery can pay its shareholders this year and what is dividend payout ratio of the company? Assume the Residual Dividend Payout Policy applies.

b) If the company is paying a dividend of $2.50/share and tomorrow the stock will go ex-dividend. Calculate the ex-dividend price tomorrow morning. Assuming the tax on dividend is 15%.

c) Little Equipment for Hire is a subsidiary in the Giant Machinery and currently under the liquidation plan due to the severe contraction of operation due to corona virus. The company plans to pay total dividend of $2.5 million now and $ 7.5 million one year from now as a liquidating dividend. The required rate of return for shareholders is 12%. Calculate the current value of the firm’s equity in total and per share if the firm has 1.5 million shares outstanding.

Answer

Week 6

a) Computation of bond price

The corporate bond price mentioned herein finance assignment can be estimated by computing the present value of the future cash flows arising from the bond which would include repayment and coupon payment.

Corporate bond face value = $ 1,000 Coupon paid annually = Coupon rate* Face value = 10%*$1,000 = $100 The maturity period of the bond is 20 years and YTM is given as 12%.

The PV of annuity formula is shown below.

PV = P*(1- (1+r)-n)/r

Where P= Periodic payment = $ 100

r = Rate of interest = 12%

n = Number of time periods = 20

Present value of the stream of future coupon payments =

100*(1-1.12-20)/0.12 = $746.94

The following formula can be used to estimate the PV of a future cashflow.

PV = FV/(1+r)n

FV = Future value = $1,000

r = Rate of interest = 12%

n = Number of time periods = 20

Present value of the bond face value received at maturity = (1000/1.1220) = $103.67

Current price of bond = $746.94 + $103.67 = $850.61

b) Computation of share price

The dividend discount model would be used for computation of share price.

Current share price = (Dividend next year)/(Rate of return – Dividend growth rate)

Dividend to be paid next year = $8.5*(1+0.04) = $ 8.84

Rate of return for the stock = 9%

The constant dividend growth rate has been given as 4%.

Present price of ordinary share of company = $8.84/(0.09 -0.04) = $176.80

c) Computation of preference share price

Dividend paid on each preference share = Expected return * Par value = (12/100)*100 = $12

Return expected from the preference share = 10% Let the current price of preference share be $X Therefore, 10% = ($12/X) Solving the above, we get X = $120

Week 7

a) NPV Computation

NPV = -CF0 + CF1/(1+r) + CF2/(1+r)2 +CF3/(1+r)3 +CF4/(1+r)4 +CF5/(1+r)5

For Project 1, CF0 = $175,000, CF1= $76,000 CF2 = $83,000 CF3 = $67,000, CF4 = $85,000, CF5 = $55,000, r = 9%

NPV (Project 1) = -$175,000 + ($76,000/1.09) + ($83,000/1.092) + ($67,000/1.093) + ($65,000/1.094) + ($55,000/1.095) = $98,114.37

For Project 2, CF0 = $185,000, CF1= $87,000, CF2 = $78,000 CF3 = $69,000, CF4 = $65,000, CF5 = $57,000, r = 9% NPV (Project 2) = -$185,000 + ($87,000/1.09) + ($78,000/1.092) + ($69,000/1.093) + ($65,000/1.094) + ($57,000/1.095) = $98,841.94 Since project 2 has a higher positive NPV, hence it would be preferred over project 1.

b) Project 1

Upfront cost = $ 175,000

The cumulative cashflows become positive in the third year. During the first two years cash inflows = $76,000 + $83,000 = $159,000

Payback period = 2 + (175,000- 159,000)/67,000 = 2.24 years

Project 2

Upfront cost = $185,000

The cumulative cashflows become positive in the third year. During the first two years cash inflows = $87,000 + $78,000 = $165,000

Payback period = 2 + (185,000 -165,000)/69,000 = 2.29

In terms of payback period, project 1 is superior since it has a lesser payback period when compared with project 2. However, permissible payback period have to be less than 2 years which is not true for any project. Hence, neither of the projects are acceptable.

c) In case of the two methods conflicting with each, project selection by Giant Machinery should be done in accordance with the superiority of the NPV. Amongst the two capital budgeting techniques used, the superior technique is NPV since payback period fails to consider the time value of money and also does not consider the entire cash flows.

Week 8

Since the debt to equity is 0.45, hence weight of debt (wd) in capital structure = (0.45/1.45) = 0.3103

Weight of equity (we) = 1 – wd = 1- 0.3103 = 0.6897

Cost of equity (ke) is given as 17.6%

Let the post tax cost of debt be kd

Cost of equity = wd*kd + we*ke

Thus, 13.5 = 0.3103*kd +0.6897*17.6

Solving the above, kd = 4.39%

Cost of debt before tax = Cost of debt post tax/(1-T)

Here, T = 35%

Hence, cost of debt before tax = 4.39%/(1-0.35) = 6.75%

Week 9

a) Market value computation

Ordinary shares market value = Number of ordinary shares * Price per share = 35,000*$47 = $1,645,000

Preference shares market value = Number of preference shares * Price per share = 5,000*$58 = $290,000

Bonds market value = Face value * Price per bond = (102/100)*$450,000 = $459,000

Firm market value is the sum of all the three securities listed above.

Hence, market value = $1,645,000 + $290,000 + $459,000 = $2,394,000

b) Weights Computation

Ordinary shares weight = (Market value of ordinary shares/ Market value of firm) = ($1,645,000/$2,394,000) = 68.71%

Preference shares weight = (Market value of preference shares/ Market value of firm) = ($290,000/$2,394,000) = 12.11% Bonds weight = (Market value of bonds/ Market value of firm) = ($459,000/$2,394,000) = 19.17%

c) WACC Computation

For ordinary shares, the cost of equity (ke) has been given as 13.5%

For preference shares, the cost of equity (kp) = (Preference Dividend/Current Market Price) = ($7/$58) = 12.07%

For bonds, the post tax cost of debt (kd) = Pre-tax cost of debt*(1-Tax) = 8.49%*(1-0.30) = 5.94%

WACC = weke + wp*kp + wd*kd

Putting the respective inputs from Part b and Part c, we get WACC = (0.6871*13.5%) + (0.1211*12.07%) + (0.1917*5.94%) = 11.88%

Week 10

a) In accordance with the residual payout policy, dividend paid should comprise of the remaining earnings after deduction of capital expenditure from the earnings.

Assuming the existing capital structure is retained, it would indicate that for capital expenditure in the future, 65% of the funds have to be put in by the company as equity.

For the estimated capital expenditure of $ 175,000 next year, the equity component would be $175,000*65% = $113,750

As a result, any money remaining after keeping the above amount aside would be paid as dividend. Thus, dividend amount = $250,000 - $113,750 = $136,250

Expected dividend payout = (Dividend paid/Actual Earnings) = (136250/250000) = 54.50%

b) Dividend per share after tax = Pre-tax dividend *(1- Tax) = $25*(1-15%) = $2.13

Ex-dividend price expected = Share price before dividend –Dividend per share after tax = $ 25 - $2.13 = $22.87

c) Current dividend amount is $2,500,000

After one year, the liquidating dividend amount = $7,500,000

Rate of return = 12%

PV of liquidating dividend amount = FV/(1+r) = ($7,500,000)/1.12 = $6,696,428.57

PV of the equity of the firm = $2,500,000 + $6,696,428.57 = $9,196,428.57

Total shares outstanding = 1,500,000

PV of equity on a per share basis = ($9,196,428.57/1,500,000) = $6.13

The providing of liquidating dividend after on year would imply that the firm does not intend to pay future dividends.