Financial Analysis Assignment: Financial Statements Evaluation of Samsung Plc

Question

Task: Pietro Yon, a local businessman, owns and manages a number of retail stores that sell a range of homewares.

Pietro is a member of the local business Chamber of Commerce and has been asked to chair a committee to research and study the success of Samsung PLC. The Chamber believes that there may be some useful learning from this study which members of the Chamber could use.

In this financial analysis assignment, you have been asked to provide specialist support to the committee and you are required to produce a range of materials for members of the committee to use.

You have been provided with the following link to view Samsung PLC’s annual reports and investor information.

https://www.samsung.com/global/ir/financial-information/audited-financial-statements/

Task 1 – Financial Data and Strategic Decision Making

You must produce a presentation for Pietro Yon to use at the next meeting of the Chamber of Commerce. The presentation should be based on your research of Samsung PLC and other relevant information. It must be accompanied by supporting notes.

Your presentation must include the following:

• An evaluation of the sources of financial data which can be used to inform business strategy.

• An assessment of the need for financial data and information in relation to the formulation of business strategy.

• An analysis of the risks related to financial business decisions.

• A review of methods that can be used for appraising strategic capital expenditure projects and strategic direction.

Task 2 – Discussion Paper

A meeting has been arranged with Pietro Yon and other members of the committee and you have been asked to produce a paper for discussion which provides:

• An interpretation of the financial statements of Samsung PLC to assess the current viability of the organisation.

• A comparative analysis of financial data using ratio analysis for Samsung PLC. You are advised to download consecutive year’s accounts from the Samsung PLC website.

Extension activities:

To gain a merit grade you must add further sections to your discussion paper that:

•Makes recommendations to Samsung PLC based on your analysis and interpretation of the financial position.

Task 3 – Information Leaflet

Extension activities:

To gain a merit grade you must produce an information leaflet for the Chamber of Commerce to distribute to the members. The leaflet should assess the following:

• The impact of ‘creative accounting’ techniques when making strategic decisions. grade you must produce an information leaflet for the Chamber of Commerce to distribute to the members. The leaflet should assess the following:

• The limitations of ratio analysis as a tool for strategic decision making.

• The importance of cash flow management when evaluating proposals for capital expenditure.

To gain a distinction grade you must prepare an additional section for the leaflet that:

• Recommends, with justifications, methods and tools that allow businesses to analyse financial data for strategic decision making purposes.

Task 4 – Capital Expenditure Appraisal

Pietro Yon has been supplied with information from a component manufacturer who has asked for advice on the best project to accept for the purchase / replacement of a piece of machinery.

The company are considering selling their old machine that has a capital cost of £260 000 and replacing it with an up to date model costing £220 000. For immediate purchase the company will receive £120 000-part exchange allowance.

Both the current and new machines are able to meet the expected company demand, estimated at:

After three years, it is predicted that demand will be zero due to the technological developments in the industry.

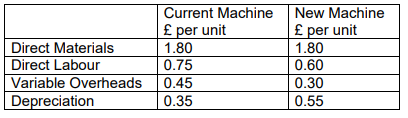

The following data has been provided for the existing and new machine:

Additional information:

(1) The selling price for each component is £5.00 and this will remain constant for the next three years. Additional information

(2) The company expect the cost of direct materials and direct labour to increase by 5% each year. (3) The company predicts that repair and maintenance costs for the current machine will be £7000 per annum.

(4) The current machine is expected to have a zero-residual value at the end of year 3.

(5) The company predicts that repair and maintenance costs for the new machine will be £1000 per annum.

(6) The new machine is expected to have a £75 000 residual value at the end of year 3.

The company’s cost of capital is 15%

Extract from the present value table for £1 at 15%

Year Units

1 0.870

2 0.756

3 0.658

4 0.572

Pietro would like you to produce a business report that can be given to the company offering advice on the best course of action for the purchase / replacement machine.

REQUIRED

Prepare a report that evaluates the capital expenditure proposals using appropriate financial techniques.

Extension activities:

To gain a distinction grade you must include an assessment of the impact of the business proposal on the strategic direction of the organisation.

Answer

Introduction

The Samsung group, focused herein financial analysis assignment, is a multinational manufacturing organisation that is headquartered in Seoul, South Korea. It is the largest South Korean business organisation which is run as the eighth highest global brand value for the year 2020. It is a private conglomerate business which was founded 83 years ago in Daegu. It operates to serve the global consumer segment and deals with providing clothing, consumer electronics, medical equipments, automotive, semiconductors, solid-state drives, home appliances, advertising, financial services, hospitality, retail, shipping building, information and communication technology, etc. It entered the electronics industry in the year 1960s and the construction industry in the 1970s.

This financial analysis assignment focuses on analysing and evaluating the financial statements of the organisation for a period of two years ending 2020 and 2019. The major financial statements to be analysed include statement of cash flows, statement of income and statement of financial position ending for the respective two financial years. Analysing financial statements include forming thesis for intra-firm and inter-firm comparisons. this assignment has been divided into four sections. The 1st section deals with assessing the various sources of gathering financial data for the organisation and assessing its worth towards determining the financial position of the entity. The second section deals with analysing the financial statements on a two-year basis and commenting on the viability and longevity of the organisation through ratio analysis, comparative income statement and balance sheet. The third section deals with the importance of creating accounting techniques in recent times, tools required for financial analysis and data comparison, discussing the limitations of ratio analysis and how it affects strategic decision making policy, the importance of cash flow management in capital budgeting decisions and proposals, and several tools required for making efficient financial statement analysis.

Task 1

Question 1

Financial statements can be described as those written records that represent the business activities, the financial performance and the economic growth of the business organisation. Often undergone through auditing process by specific experts and accountants, these financial statements form a part of financial reporting framework that ensures fairness, relevance and accuracy of information contained in it. There are three major financial statements that include balance sheet, income statement and the cash flow statement of the organisation. Potential and current investors and other financial analysts are heavily reliant on such financial data to analyse and evaluate company performance and make business valuation predictions about the stock prices of the entity. These statements are used by both internal and external stakeholders to assess the financial health and earning potential of the organisation.

1. Balance sheet or the statement of financial position is an apprehensive statement that briefly discusses all the liabilities whether short-term or long-term, the assets owned by the business whether current or non-current and the equity component of the business. Equity component open includes paid-up capital, retained earnings, profit and loss account, general reserve and other similar reserves created out of undistributed past profits. Data that is retrieved from balance sheet include cash and equivalence, trade receivables, trade payables, inventory in stock, shareholders equity, retained warnings, long-term borrowings, etc.

2. Income statement is a representation of the income generated through the operational performance of the business. This statement covers all the income and expenses that accrue to the organisation for the financial year. If an organisation undertakes basis of accounting, all those income earned and expenses incurred will be represented that have accrued for the financial year irrespective of its cash receipts or payments. On the other hand, if cash basis of accounting is adopted, all such income and expenses will be recorded that have actually been received or paid irrespective of it accrual tendency

3. Cash flow statement can be described as a brief representation of how cash is managed under the three sections namely operating activities, investing activities and financing activities. It signifies and measures how well an organisation is able to generate cash and equivalent to meet debt obligations and finance its operating requirements. The data collected from this statement allows the stakeholders in assessing the smooth operation of performance of the business and its money generating capacity to meet current operational needs. The operating activities of the statement include cash generated or utilised in running the business. The investing activities include all sources where the money has been invested into or generated from the purchase or sale of long-term assets. Financing activities include all sources where cash is generated or utilised to finance the business. It includes issue of debt, buyback of equity, dividend payments and debt repayment.

The given case scenario of Samsung PLC.is an organisation that produces statements in the form of cash flow statement, income statement, statement of financial position and statement of other comprehensive income. All these financial statements are very sources where the financial data of the organisation is extracted from and is utilised by both the internal and external stakeholders to review the financial and operational efficiency of business performance for the relevant financial year.

Question 2

Business strategies can be defined as a thoughtful process that allows the business to perform in a particular manner to meet its goals in objectives with diligence and conformity with regulations. After understanding the financial health of the business, the management decides to undergo a strategic planning process to allocate its limited resources towards meeting predetermined objectives of the business. It helps to assess the net cash available to the business. The importance of cash as an asset to the company is already known. It is used to generate and allow operational efficiency with smoothness without creating any hurdles in the business. Financial data represents the revenue growth of the organisation. This is an important determinant for the business management to and taps the potential success of the business and makes strategic planning accordingly. Profit earning capacity of the business is likely to be evaluated and compared with the peers in the industry and also with the organisation itself by comparing the same with the past financial periods. Hence with the intention to improve and meet the industry power, it is important to set such strategies that are effective in accelerating operational performance and financial growth for the organisation. Financial statements not only major operation efficiency of the business resources, but also is a great contribute to towards measuring economic value added. It is hence very helpful in making timely decisions about business expansion and strategically undertake such actions that could be corrective in nature to uplift the diminishing economic value added so generated. Financial analysis metrics are highly effective in meeting and assessment to the internal strengths and weaknesses and the external opportunities and threats available Ano associated with the organisation. This internal and external evaluation of the company provides the management with adequate information in formulating strategies and decisions under priority basis and maximising the competencies of the organisation.

Examples include:

1. SWOT ANALYSIS: CORE COMPETENCIES, INTERNAL AND EXTERNAL WEAKNESS AND OPPORTUNITIES

2. PESTLE ANALYSIS: EXTERNAL ENVIRONMENTAL FACTORS ANALYSIS

3. BALANCE SHEET: STATEMENT OF LIABILTITIES AND ASSETS

4. INCOME STATEMENT: PROVIDES NET PROFITS AND OPERATING PROFITS

Question 3

Risk and rewards are two sides of the same coin named business. The greater the risk, the higher is the probability of getting rewarded. On the contrary, if the risk is lover it is probable that the rewards will also be lower. With respect to financial business decisions, some of the risk that any organisation may face a listed as under-

a. Strategic risk – this type of risk arises when a business organisation does not operate as per the defined business model components. When any organisation fails to meet its operational business model, it is quite likely that the strategy would become ineffective to reach its predetermined goals. Hence, when operational performance does not meet the benchmark so set, it is likely the business decision shall be adversely affected

b. Compliance risk – when any business organisation raises funds in the form of equity, debt specifically, it is important to comply with the necessary legal and regulatory requirements. This is Sewden because it is important to protect the funds of the real owner and their interests as well with growing awareness to protect the needs and expectations of the investors, meeting compliance and security requirements have become a mandate. Hence exposing an organisation to compliance risk can be stressful for undertaking effective financial business decisions

c. Reputational risk-this is one of the most important risk that any organisation is exposed to. If a company due to any business inefficiency or ineffective performance is exposed to reputational loss under any circumstance, it is likely that it would affect the business decision on financial grounds.

Question 4

The strategic decision tools required for capital expenditure projects are given as under-

A. NPV - net present value is one of the most popularly used methods to assess the viability of any given project. It allows to considers time value of money by discounting the cash flows both inflows and outflows using a specific rate usually the cost of capital rate.

B. IRR – Internal rate of return is the hurdle rate where present value of cash inflows equals the present value of cash outflows. Return on project should always be more than IRR.

C. PAYBACK PERIOD – it is described as the span when the recovery of initial investment is completely been made.

D. Discounted PAYBACK PERIOD – it is described as the span when the recovery of initial investment is through inflows from the project discounted at the hurdle rate been made

Task 2: Discussion Paper

Analysis

|

SAMSUNG PLC: VERTICAL ANALYSIS |

||||

|

Particulars |

2020(KRW) |

% |

2019(KRW) |

% |

|

REVENUE |

236,806,988 |

100.00% |

230,400,881 |

100.00% |

|

COST OF SALES |

144,488,296 |

61.02% |

147,239,549 |

63.91% |

|

GROSS PROFIT |

92,318,692 |

38.98% |

83,161,332 |

36.09% |

|

SELLING AND ADMINISTARTIVE EXPENSES |

56,324,816 |

23.79% |

55,392,823 |

24.04% |

|

OPERATING PROFIT |

35,993,876 |

15.20% |

27,768,509 |

12.05% |

|

OTHER NON-OPERATING INCOME |

134,068 |

0.06% |

1,778,666 |

0.77% |

|

OTHER NON-OPERATING EXPENSE |

2,488,902 |

1.05% |

1,414,707 |

0.61% |

|

SHARE OF NET PROFIT OF ASSOCIATE |

506,530 |

0.21% |

412,960 |

0.18% |

|

FINANCIAL INCOME |

12,267,600 |

5.18% |

10,161,632 |

4.41% |

|

FINANCILA EXPENSE |

11,318,055 |

4.78% |

8,274,871 |

3.59% |

|

PBT |

36,345,117 |

15.35% |

30,432,189 |

13.21% |

|

INCOME TAX EXPENSE |

9,937,285 |

4.20% |

8,693,324 |

3.77% |

|

PAT |

26,407,832 |

11.15% |

21,738,865 |

9.44% |

The above information after drawing down the vertical analysis is clear in representing that the total cost of sales for the organisation has decreased by 3% then last year with the respective increase in its gross profit from 36% in the year ending 2019 to 39% in the year ending 2020. Operating expenses have also increased by 3% than last year. There has been a significant increase in the profit after taxes from 9% in 2019 to 11% in 2020.

|

Ratio Analysis |

2020 |

2019 |

|

CURRENT ASSETS |

198,215,587 |

181,385,260 |

|

CURRENT LIABILITIES |

75,604,351 |

63,782,764 |

|

LIQUID ASSETS |

163,906,342 |

152,212,576 |

|

(CURRENT ASSETS-STOCK-PREPAID EXPENSES) |

|

|

|

LIQUID LIABILITIES |

75,604,351 |

63,782,764 |

|

(CURRENT LIABILITIES-BANK OVERDRAFT) |

|

|

|

|

|

|

|

CURRENT RATIO |

2.62 |

2.84 |

|

LIQUID RATIO |

2.17 |

2.39 |

|

|

|

|

|

TOTAL DEBT |

26,683,351 |

25,901,312 |

|

TOTAL EQUITY |

275,948,016 |

262,880,421 |

|

TOTAL ASSETS |

378,235,718 |

352,564,497 |

|

|

|

|

|

DEBT EQUITY RATIO |

0.10 |

0.10 |

|

DEBT TO TOAL ASSET RATIO |

0.07 |

0.07 |

|

|

|

|

|

GROSS PROFIT |

92,318,692 |

83,161,332 |

|

NET PROFIT |

26,407,832 |

21,738,865 |

|

REVENUE |

236,806,988 |

230,400,881 |

|

|

|

|

|

NET PROFIT MARGIN |

11.15% |

9.44% |

|

GROSS PRFOIT MARGIN |

38.98% |

36.09% |

|

|

|

|

An ideal current ratio is two times. An ideal quick ratio is one times. The company has been able to maintain a stable current ratio and liquidation. This signifies that the company is able to manage its cash levels very well and efficiently and is in a position to effectively discharge its short-term obligations to meet operational demands. A debt equity ratio or a debt to total asset ratio less than one is considered to be the best. The ratio for both the years is almost the same and under acceptable limits. Net profit margin has increased along with a significant increase in the gross profit margin of the organisation.

Recommendations

Although the financial performance of the organisation has remained quite stable and well with respect to the previous years, some recommendations and suggestions can be incorporated to enhance it further. These are provided as under-

a. Since the company is already in established brand, it can undertake measures to reduce its fixed cost with respect to selling and advertisement expense

b. With increased sales, the company is also facing increased cost. Hence the management is required to work more towards reducing operating expenses so as to enhance the profitability margins

Task 3: Information Leaflet

Part 1: Impact of ‘creative accounting’ techniques on strategic decisions

Creative accounting can be described as a set of accounting practises that confirm to required legislative and compliance regulations but cause to deviate from what intended accounting standards mean to achieve. Hence, these accounting practices focus on creating loopholes in the established accounting standards to present a far better financial and non-financial image of the organisation. This representation is false, and fair and misleading to the investors. Hence, it can be said that creative accounting practises distort the true business value of the enterprise by providing misleading financial information to its internal and external stakeholders.(Amat, (1999)) These creative accountants enjoy taking the company on the upside and reflecting it as profitable by twisting the true financial information. Running on this risk, many business organisations try to meet their short-term objectives quite quickly with a significant increase in its share prices. It also helps for example the lenders to give the organisation a prospective amount of loan which it would otherwise had not been convinced if it had relied on true financial information. The various types of creative accounting practices include over estimating the revenues of several business organisations, undercharging depreciation expenses, etc. Adopting such accounting policies can allow the management to make strategies that focus on accelerating the financial image of the company. (Wokukwu, March 2015)

Part 2: Limitations of ratio analysis as a tool for strategic decision making

Ratio analysis is considered to be one of the most popular techniques in analysing the financial statements of a business organisation. It extracts financial information from the statements and visualise various profitability, efficiency, solvency and liquidity situation of the business. Like every coin has two sides, there are both advantages and limitations to ratio analysis that an organisation is likely to face. Some of the crucial limitations that are associated with ratio analysis in making effective strategic decisions are described as under- (Faello, January 2015)

1. Information used in ratio analysis is based on historical data. Although past information can be useful for laying down trends for the organisation, these metrics not necessarily are reliable enough to represent the performance of the organisation in future. It means cause the management to undertake strategies that will prove to be ineffective in future for the business

2. Financial statements are periodically released and hence there exist significant time lag across each release date. If there is an inflation existing between these periods, the statements presented do not reflect the real prices that could affect financial position of the business. Hence, Ratio analysis do not provide reliable information for strategic decision making as it does not take inflation into account. Strategies are considered to be highly effective when did taken to consideration future economic and monetary policies.

3. Ratio analysis does not take into account if there are changes in accounting policies adopted by the organisation. Even if such accounting policies reflecting the financial statements, they become incomparable when ratio analysis is done and hence proper strategy is cannot be developed on the basis of un comparable data(INSTITUTE, 2019)

Part3: Importance of cash flow management when evaluating proposals for capital expenditure

A capital expenditure proposal is a non-expenditure which is associated with purchasing or constructing any facility or equipment. It requires a formal plan to be laid down that lists various necessary resources required for the proposal to be operational. The investment is best assessed and evaluated with the cash inflows forecasted to be generated during the life of investment. These estimated inflows take into account any inflation rate, change in demand and production levels, etc. different capital budgeting techniques like profitability index, accounting rate of return, payback period, internal rate of return and net present value or solely based on the cash flows and, management of such cash flows are extremely important for taking effective and efficient capital budgeting decisions. These decisions calculate whether the cash flow generated after taxes and discounted killed a positive result all are capable of generating profits after the recovery of investment over the life of the project. The cash basis approach of evaluating the viability of such projects helps in undertaking profitable investment decisions that would accelerate the financial performance of the business.

Cash is considered to be an important business resource for the organisation and hence is management is extremely crucial for meeting the daily operations of the business. Capital expenditure proposals require initial investment to be made which is large some outflows to be made that are constant irrespective of the level of production. Hence, cash management is important not only at the initial stage of investment but through the project span as well to maintain day to day operation of the business (Tuner, 2016)

Part 4: Methods and tools that allow businesses to analyse financial data for strategic decision-making purposes

Financial statement analysis is a very crucial process as it involves in evaluating and assessing the financial information contained in the financial reports of an organisation. It helps to under the financial status of the entity and make both intra firm and inter firm comparisons. Important tools and techniques that aid in the analysis of such financial statements are provided as under-

a. Comparative statement-these deals with comparing several aspects of the statement of financial position and the income statement Concerning toward more financial fears of giving business organisation. Different comparative statement prepared each for the income statement and for the statement of financial position. It helps in analysing the financial growth of the organisation with respect to its financial position and profits thereby making intra firm comparisons.

b. Common size statement-this is a vertical representation of the financial information contained in the statement of financial position. The total assets are considered to be hundred and likewise a percentage is calculated for each aspect of information contained in the balance sheet. Likewise, comparative statement of the day, these statements are also prepared separately for both income statement and statement of financial position.

c. Trend analysis- it is an analysis methodology where relations of different items are prepared and analysed and then compared to form and comment on the train weather or downwards. This evaluation methodology is also known as the pyramid model. It gives a clear picture about the financial position of the business trending up the slope or down.

Task 4: Capital Expenditure Appraisal

Details of old machine

|

Old machine |

|

|

|

|

|

|

|

|

|

|

|

Particulars (Years) |

0 |

1 |

2 |

3 |

|

Output |

|

90000 |

50000 |

30000 |

|

Investment |

220000 |

|

|

|

|

Sales |

|

450000 |

250000 |

150000 |

|

Less: |

|

|

|

|

|

Direct material |

|

162000 |

94500 |

59535 |

|

Direct labour |

|

67500 |

39375 |

24806.25 |

|

Variable overheads |

|

40500 |

22500 |

13500 |

|

Depreciation |

|

31500 |

17500 |

10500 |

|

Maintenance costs |

|

7000 |

7000 |

7000 |

|

Operating cash flow before taxes |

|

141500 |

69125 |

34658.75 |

|

Less : taxes |

|

0 |

0 |

0 |

|

Operating profit after taxes |

|

141500 |

69125 |

34658.75 |

|

Post tax salvage value |

|

|

|

0 |

|

Add: depreciation |

|

31500 |

17500 |

10500 |

|

Cash flow after taxes |

220000 |

173000 |

86625 |

45158.75 |

|

PVIF |

1 |

0.87 |

0.756 |

0.658 |

|

PV |

220000 |

150510 |

65488.5 |

29714.4575 |

|

|

|

|

|

|

|

Net Present Value |

25712.9575 |

|

|

|

|

|

|

|

|

|

|

Investment |

220000 |

|

Depreciation for 3 years |

59500 |

|

Book value |

160500 |

|

Salvage value |

0 |

|

Profit |

-160500 |

|

Tax savings on loss |

0 |

|

Post tax salvage value |

0 |

|

|

|

Details of new machine

|

New machine |

|

|

|

|

|

|

|

|

|

|

|

Particulars |

0 |

1 |

2 |

3 |

|

Output |

|

90000 |

50000 |

30000 |

|

Investment |

140000 |

|

|

|

|

Sales |

|

450000 |

250000 |

150000 |

|

Less: |

|

|

|

|

|

Direct material |

|

162000 |

94500 |

59535 |

|

Direct labour |

|

54000 |

31500 |

19845 |

|

Variable overheads |

|

27000 |

15000 |

9000 |

|

Depreciation |

|

49500 |

27500 |

16500 |

|

Maintenance costs |

|

1000 |

1000 |

1000 |

|

Operating cash flow before taxes |

|

156500 |

80500 |

44120 |

|

Less : taxes |

|

0 |

0 |

0 |

|

Operating profit after taxes |

|

156500 |

80500 |

44120 |

|

Post tax salvage value |

|

|

|

75000 |

|

Add: depreciation |

|

49500 |

27500 |

16500 |

|

Cash flow after taxes |

140000 |

206000 |

108000 |

135620 |

|

PVIF |

1 |

0.87 |

0.756 |

0.658 |

|

PV |

140000 |

179220 |

81648 |

89237.96 |

|

|

|

|

|

|

|

Net Present Value |

210105.96 |

|

|

|

|

|

|

|

|

|

|

Investment |

140000 |

|

Depreciation for 3 years |

93500 |

|

Book value |

46500 |

|

Salvage value |

75000 |

|

Profit |

28500 |

|

Tax on profit |

0 |

|

Post tax salvage value |

75000 |

Assumptions

1. It is assumed that the organisation is not attracted to paying corporate taxes to the government. In the absence of any given information, it is assumed that the entity is that exempt

2. Since the depreciation amount is changing with the number of units produced, it is assumed that the accounting policy of charging depreciation adopted by the organisation is written down value method of depreciation the depreciation charges reduced with every passing year.

Payback period shall be calculated using interpretation method

a. Old machine-

(c-1)/(2-1) = (220000-173000)/(259625-173000) = 1.54 years

The investment will be recovered within a period of 1.54 years

b. New machine

x-0/(1-0) = (140000-0)/(260000-0) = 0.53 years or 6.5 months

The investment will be recovered within a period of 6.5 months

Accounting rate of return is calculated by dividing present value of inflows with the present value of the outflows. The higher the rate, better is the efficiency of the project

a. Old machine- 245713/220000 = 1.12

b. New machine = 350106/140000 = 2.50

Results of the analysis

From the calculations and analysis provided as above, it is quite clear that the net present value generated by the new machine is far better and enhanced than the value generated by the old machine. Not only does it provide increased net present value over the years, the new machine project is likely to recover the investment within a period of seven months. Also the accounting rate of return of the old machine is 2.5 times versus 1.12 times of the old machine. Hence, it would be suggested that the company continues its policy to adopt the new machine and scrap of the old one to reap competitive advantage within the industry and gain maximum benefits through increased operational efficiency and accelerated financial performance.

Bibliography

Amat, O. &. ( (1999)). The Ethics of Creative Accounting. . RePEc .

Faello, J. (January 2015). Understanding the limitations of financial ratios. Academy of Accounting and Financial Studies Journal 19(3) , 75-86.

INSTITUTE, C. F. (2019). Limitations of Ratio Analysis. https://corporatefinanceinstitute.com/resources/knowledge/finance/limitations-ratio-analysis/ .

Tuner, J. A. (2016). Net Operating Working Capital, Capital Budgeting, and Cash Budgets: A Teaching Example. Financial analysis assignmentAmerican Journal of Business Education, v9 n1 , 15-22 .

Wokukwu, D. K. (March 2015). Creative Accounting: Unethical Accounting and Financial Practices Designed To Boot Earnings and To Meet Financial Market Expectations. Journal of Business & Economic Policy, Vol. 2, No. 1; , 39-48.