Financial Assignment: A fiscal analysis of National Australian Bank

Question

Task 1: Write a report on Australian Financial Institutions. You are required to write the report in the light of main types of financial institutions as classified by the Reserve Bank of Australia.

Task 2: Write a report on the performance of a major bank in Australia. You are required to write the report using the information from the Annual Report of the Bank, Australian Prudential Regulation Authority, Reserve Bank of Australia, DataAnalysis Premium, and other relevant resources.

Task 3: Write a report on the term structure of interest rates in Australia. You are required to write the report using from the Reserve Bank of Australia and other relevant resources.

Answer

The main types of financial institutions classified by the RBA as discussed in this financial assignment are as follows:

Depository institutions – Also termed as banks are present in the form of commercial banks, savings, loans, receipt of money from the depositors to lend to the borrowers. The main function of the depository as discussed in this finance assignment report is to provide services that are sound and ensure liquidity. Secondly, it provides a system of payment that comprises of electronic funds transfer. Thirdly, the money of the savers is pooled and let out to the people and business (Phillipsiney & Phillips, 2015). Lastly, they even invest in securities.

Investment banks – It is an organization that provides financial services or corporate division that is engaged in financial transactions that are advisory based on behalf of individuals, companies, and government. Investment banks assist the companies that are involved in merger and acquisitions and provide other services that are ancillary in nature. Such services comprise of services relating to equity and derivatives. It needs to be noted that most of the investment banks keep department of prime brokerage and asset management that is in tune with the investment research services (Phillipsiney & Phillips, 2015).

A contractual saving institution such institution in Australia comprises of provident funds, insurance companies, pension funds, etc. When it comes to the point of term finance, such an institution can be tagged as the ideal one owing to the presence of long term liabilities and stable cash flows (RBA, 2018). Such an institution is of major help not only to the government and industry but even to the housing sectors. It plays a predominant role in shaping the economy of Australia.

Finance companies – There are a different variety of finance companies as observed in this finance assignment report that help in proving loans or finance to other customers. Some finance companies provide loans to business while some to the customers. As they do not take deposits from the public they do not come under the ambit of banks and they are not required to meet the banking regulations (RBA, 2018). The finance companies procure funds for lending through borrowing from the parent corporation.

Unit Trust – It is a major way of collective investment in Australia that is constituted under a trust deed. A unit trust pools the money of the investors into a single fund that is managed by the manager of the fund. It provides access to a variety of investment and resting on the trust it might invest in securities like shares, binds and other forms of properties like mortgages and equivalents of cash (Phillipsiney & Phillips, 2015). When the investment is done in the trust own units, the price is termed as net asset value. The number of such units is not fixed and when more gets invested in a unit trust then more units are bound to be created.

Answer 2

National Australia Bank (NAB) performance failed to match the expectations of all investors as its cash earnings reported a huge decline of 14.2% and reported at $5702 million that is a negative indicator of its performance especially when compared with its rivals like Australia and New Zealand Banking Group (ANZ). Furthermore, many believed that this was still an effective outcome on the part of NAB considering the complicated trading conditions in the market but, the bank had completely fallen below expectations. In addition, the company’s underlying profit fell to $8985 million that was 14.2% lesser in comparison to the previous year (NAB, 2018). This observation in this financial services assignment sheds light on the fact that the share prices of NAB will be more likely to suffer from deterioration very soon.

Such underperformance of the company was because of its segment of Consumer Banking and Wealth that had depicted a 5.8% decline in the cash earnings wherein it reported at $1.539 million. Furthermore, the reason behind such underperformance as observed in this financial services assignment can be attributed to a massive deterioration in the housing margin of the company that had been caused by huge competition in the market and variation in the lending mix. In addition to this, the segment of Business and Private Banking of the company’s performance was also offset and that resulted in an increment of cash earnings of 2.5% that reflected at $2911 million (NAB, 2018). Nevertheless, the management had suggested that this depicted effective lending of SME business and greater margins. Moreover, its performance could have been better if it had not been offset by increasing operating costs because of the exaggeration of investments combined with the charges of greater credit impairment. The New Zealand Banking segment of the company also performed effectively as it reported a 6.7% increment in the cash earnings and reported at NZ$1004 million. Besides, the same was accelerated by greater margins and increment in lending but partly offset by exaggerated investments.

Lastly in this financial assignment, the segment of Corporate and Institutional of the bank also reported a 0.4% increment of cash earnings wherein it reflected at $1541 million. Further, the management suggested that such stagnant outcome was because of the increasing revenue on the part of non-markets and the lesser charges from credit impairment (NAB, 2018). Nevertheless, this was also offset by the declining lesser revenue from markets and exaggerated spending of investments.

The company’s net operating costs exaggerated by $1371 million that excluded costs associated to restructuring ($755 million) and customer-oriented remediation of $111 million. In addition, the company’s net operating expenses was largely driven by enhanced investments in technologies, greater amortization and depreciation expenses, enhanced marketing spend, etc. Nevertheless, these were partially offset by the benefits of productivity that included in sourcing and restructuring related with simplification of the company’s affairs and decline in the spending from third parties. In addition to this, the credit impairment charge of the company declined by $33 million that was majorly because of lesser charges of credit impairment, partially offset by the provisional charges for enhancements of mortgage model so that a better approach can be established and a lower category of collective provision can be released (NAB, 2018).

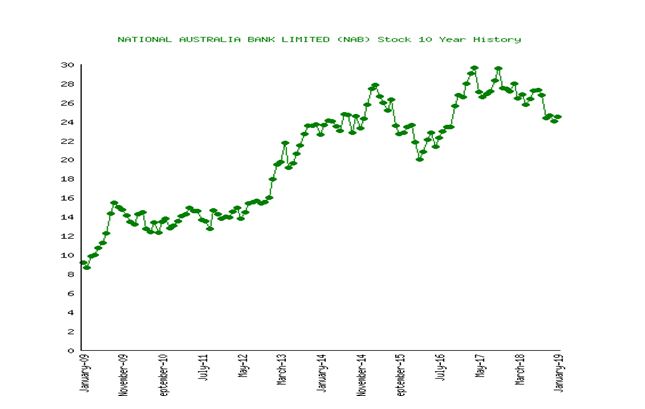

The company’s directors have also declared a final dividend of ninety-nine cents per fully paid share that amounts to $2707 million approximately. As seen above the share price hit a record high in the year 2018. Further, the Group also regularly adjusts DRP (Dividend Reinvestment Plan) so that the capital position can be reflected effectively. In addition, the company also intends to offer a 1.5% discount on such plan that has nil participation limit. In contrast to this, the company paid its final dividend of 99 cents per fully paid share in December 2017 and the same amounted to $2659 million. Besides, its interim dividend for the year ended September 2018 was paid on July 2018 itself of an amount of $2696 million (NAB, 2018).

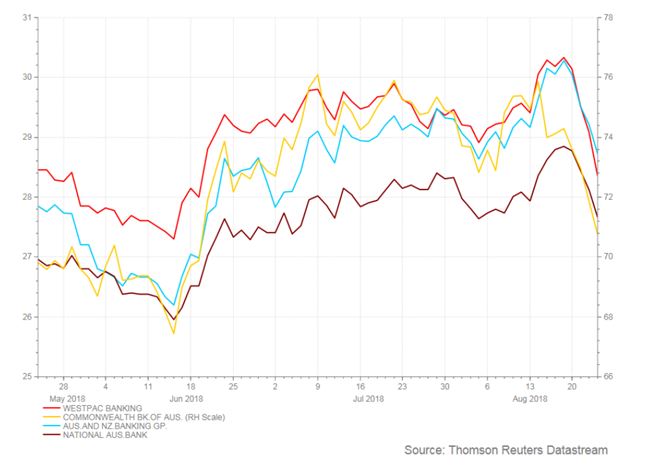

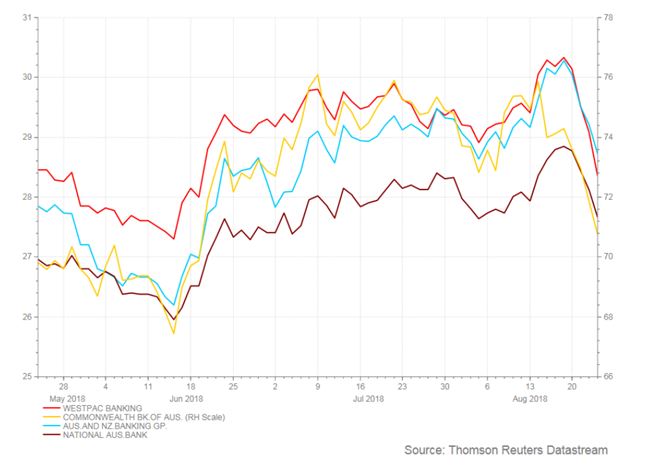

The company is vulnerable to various credit risks that can influence its goodwill in the market and financial situation as well. All lending affairs of the company play a key role in such exposure of credit risks. Further, other modes are trading and banking books, extension of guarantees and commitments, etc. In addition, the lending portfolio of the Group comprises of residential housing loans that also poses a major threat to its affairs (Mickleboro, 2019). Therefore, such credit risk can enhance in response to the disastrous economic or business situations that includes declining prices of commercial or residential properties, deterioration in the levels of employment, higher levels of household debts throughout New Zealand and Australia, and greater volatilities in the political environment of the company. The big four banks comparison has been illustrated with the help of the chart below

Answer 3

The interrelationship or connection betwixt the bond yields or rate of interests and various maturities or terms is commonly referred as the term structure of rates of interest. In other words, such term structure is also called yield curve (Peirson et. al, 2015). Moreover, such term structure of interest rate is also regarded as the most relevant benchmark that is prevalent in the world of fixed income and that is central to all the debt securities, thereby playing a very pivotal part in the overall economy. Nevertheless, the term structure depicts the collective anticipations on the part of all market players about the variations in future in relation to inflation, rates of interest, and their evaluation of situations of monetary policy. In other words, long-term rates of interest are generally determined in part by the future and present anticipated short-term rates, which is also called as forward rates, in a way that the investors remain indifferent betwixt investment in the long-term bonds and investment in a sequence of various bonds of short-term nature (RBA, 2018). It is hence observed in this financial assignment that the primary reason behind the as discussed in this financial services assignment same can be attributed to the fact that the options play a key role in returning these to the respective investors.

It was discussed in this financial services assignment that apart from the anticipations of investors, risk premia that plays a key role in compensating the investors for the deferring consumption also affects the term structure of rates of interest today. Besides, any variation in the yields can also depict variations in the expectations of term risk or because of variations in the future uncertainties associated with inflation that can influence the purchasing power on a whole (Adra & Barbopoulos, 2018). Overall, this makes the interpretation and modelling of term structure of interest rates very complicated. It was also observed in this financial assignment that Nonetheless, prices of inter-bank rates of interest, zero-coupon bonds, etc offers clue about such term structure and therefore, it is not shocking that there are various models of term structure.

References

Adra, S. and Barbopoulos, L.G. (2018) The valuation effects of investor attention in stock-financed acquisitions. Journal of Empirical Finance. [online]. 45, 108-125. Doi: https://doi.org/10.1016/j.jempfin.2017.10.001

Mickleboro, J. (2019). This is how ANZ Bank, CBA, NAB, and Westpac shares performed in 2018. Retrieved from https://www.fool.com.au/2019/01/02/this-is-how-anz-bank-cba-nab-and-westpac-shares-performed-in-2018/

NAB. (2018). NAB annual report and accounts 2018. Retrieved from https://capital.nab.com.au/docs/2018_NAB_Annual_Financial_Report.pdf

Peirson, G, Brown, R., Easton, S, Howard, P. and Pinder, S. (2015). Business Finance, 12th ed. North Ryde: McGraw-Hill Australia.

RBA. (2018). Reserve bank of Australia Bulletin. Retrieved from https://www.rba.gov.au/

Viney, C. & Phillips, P. (2015). Financial institutions, instruments, and markets. 8th ed. McGraw-Hill Australia, Sydney. ISBN: 9781743079959