Statistics Assignment: Identification of Business Problems

Question

Task: Statistics Assignment Task:

Answer

1. Business Problems: Identification

The accountants perform different activities among which reporting is considered as the most adequate. In relation to this point mentioned in the statistics assignment, "Reporting” has occurred almost 357 times in the book of accounting information system by James Hall. The accountants therefore desire to generate financial report which should be real and interactive in nature. This also should be done without any interference of the IT team (Belfo& Trigo, 2013). Henceforth this is known that at present entire world is facing the financial crisis and due to this the AIS usage by several stakeholders who are external has become more critical as well as important.

2. Information with Relevance

One of the common activities that accountants execute is Auditing. Significantly it could be found that auditing is segmented within two key divisions, one is internal auditing and another one is external auditing. In case of internal auditing it can be said that it particularly copes with widespread activities in place of the company. This widespread activity involves performing audit on the financial statements of the company as well as assessing whether the operational process in the company is aligned with compliance in accordance with the internal policies. Additionally, internal auditing process further evaluates the compliance with lawful objectivity. It further analyse the effectiveness while identifying any fraudulentactivities within the organisation (Axén, 2018). Furthermore, it can be evaluated that internal auditors requires intense assistance for executing their duties in accordance with the IT implementation.

On the other hand, in case of the external auditors, it would be found that although external auditor similarly performs most likely to the internal auditors.However, external auditors tend to be highly attentive and oriented to certain laws and legislative regulations in context to the financial statement assessment. Moreover, it is also observed that external auditors are considered as the arbitrator; however, internal auditors are considered as the members of board within the company. Significantly, auditing companies are continuously striving to identify particular process through which performance effectiveness can be enhanced.This is to be done through immensely emphasising on the core processes of the auditing and depending upon efficiency of divisions of internal auditing. Additionally, team for audit and other related performance engagement are bound to take part within the contrivance assemblies. It would simply help them in recognising the potential threats and issues that might occur within certain fraudulent activities. Thus, in terms of outcome, it is observed that auditing companies are mostly becoming IT oriented in terms of implementation of “Computer Assisted Auditing Tools and Techniques”(Pedrosa, Costa& Aparicio, 2019).

3. Methods Identification

Within the business or technological aspect, the calibration of information technology and business could be considered a key matter for the business managers in this context. The organisational success therefore could depend on the collaboration of these two matters, therefore business as well as IT throughout their several dimensions which are also multifaceted in nature. These dimensions therefore could be governance, communication, value measurements as well as technological skills or scopes. This happens because of the critical aspects of this system.

4. Reliability and Validity

Due to AIS support, the IT system has already proved to impose the positive implication of productivity and performance of different companies in this situation. Based on the viewpoint of (Esmeray, 2016) if the SME sectors and industry tend to invest on the AIS, that could easily enhance the action scope as well as also save the time. This kind of investment also increase the opportunity to deal with the bank as we as Central administration. It can be stated that if this investment on the innovation could be successful that could eventually decrease the cost of the company and enhance the productivity of the organisation.

5. Application of Statistical Tools

Statistical Technique 1: Corelation

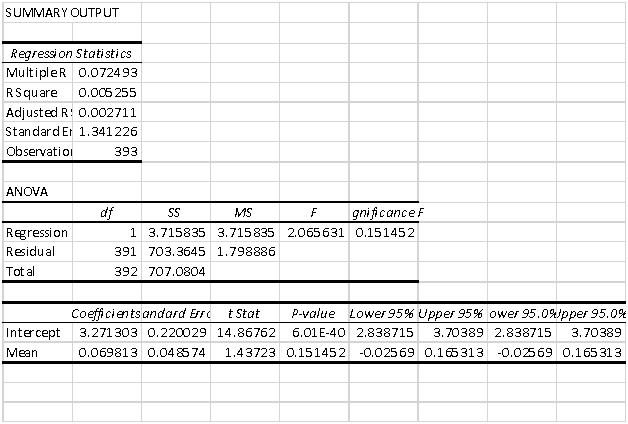

Statistical Technique 2: Regression

Statistical Technique 3: ANNOVA Test

6. Description on Technology

6.1 Estimated Correlation

In terms of estimated correlations, the followings are observed;

- Correlation-coefficients are fundamentally incorporated for quantifying robustness of connection within two of the variables.

- Moreover, Pearson-correlation has been considered as widely utilised approach within the field of statistics. It helps in quantifying the robustness alongside liner connection indication within two of the variables (Jiang, 2018).

- Valuation further reflects scale of -1 as well as +1. That is negative connection and positive connection. And, values indicating zero or near zero depicts no connectionor feeble connection.

- However, correlation-coefficients estimated lower than (+) 0.8 or more than (-) 0.8 then would not be addressed as important.

6.2 Linear programming

A. This is important to attain the maximum resource uses which should be productive in nature and in this matter linear method could help. This also depict the process through which different factors for production could be used by decision-maker by identifying and delegating those resources (Kolotilin, 2018)

B. This technique or method also enhance the decision quality as well through which the users want to accomplish objective instead of accomplishing any subjective matter

C. There can be some challenges which can create issue in system outside and for this linear method represents the proper solution. But every produced units’ docs didn't sold off and for this proper modification regarding several mathematical expression to help the decision-makers

6.3 ANNOVA Simulation

Simulators’ fundamental benefit would be the capability of facilitating users through experiential assessment while outlining real-life approaches. It would permit the originator in deciding rightness and designing effectiveness at the time of conceptualisation. User can inspect benefits of the substitutes despite constructing actual system. Furthermore, the total cost might decrease if certain design impacts are assessed at designing level instead of development level. Consideration of designing and fabrication can be expensive, specifically in terms of assessing the performance and making decisions (Bocciarelliet al. 2017). Therefore, the implementation of simulator would be highly effective. Based on it, user might inspect every outlined designby not having fabrication of circuits. By copying designing behaviour, simulators can facilitate with relevant information on rightness and efficiency for the substitutes. The cautious result of designs helps in fabricating the most effective circuit.

7. Recommendations for Technique to be used

Linear programming or method as well as LP is considered as one of the major techniques due to several causes, such as,

a) This technique provides solution for any issues within the business logically

b) Managers can take decisions based on this method of LP while considering the productivity as well as profitability

c) For the uses of resources and its allocation this technique represents several information

d) The process of LP could easily adjust within any kind of changing environment

e) If there are issues regarding multi-dimensional linear method can provides solution ?

References

Axén, L. (2018). Exploring the association between the content of internal audit disclosures and external audit fees: Evidence from Sweden. International Journal of Auditing, 22(2), 285-297. Retrieved from https://www.diva-portal.org/smash/get/diva2:1238653/FULLTEXT01.pdf [Retrieved On 08.09.2020]

Belfo, F., & Trigo, A. (2013). Accounting information systems: Tradition and future directions. Procedia Technology, 9, 536-546. [online] https://core.ac.uk/download/pdf/82811448.pdf

Bocciarelli, P., D'Ambrogio, A., Paglia, E., Panetti, T., Giglio, A., &Plinio, V. (2017, November). A Cloud-based Service-oriented Architecture For Business Process Modeling And Simulation.Statistics assignment In CIISE (pp. 87-93). Retrieved from http://ceur-ws.org/Vol-2010/paper12.pdf [Retrieved On 08.09.2020] Esmeray, A. (2016). The Impact of Accounting Information Systems (AIS) on Firm Performance: Empirical Evidence in Turkish Small and Medium Sized Enterprises. International Review of Management and Marketing, 6(2). Retrieved from https://pdfs.semanticscholar.org/f719/73eccc0911c49f8dd858f3085ef5fbfc0807.pdf [Retrieved On 08.09.2020]

Jiang, W. (2018). A correlation coefficient for belief functions. International Journal of Approximate Reasoning, 103, 94-106. Retrieved from https://arxiv.org/pdf/1612.05497 [Retrieved On 08.09.2020]

Kolotilin, A. (2018). Optimal information disclosure: A linear programming approach. Theoretical Economics, 13(2), 607-635. Retrieved from https://onlinelibrary.wiley.com/doi/pdf/10.3982/TE1805%4010.3982/%28ISSN%291468-0262.ES-cross-journal-vi [Retrieved On 08.09.2020]

Pedrosa, I., Costa, C. J., & Aparicio, M. (2019). Determinants adoption of computer-assisted auditing tools (CAATs). Cognition, Technology & Work, 1-19. Retrieved from https://repositorio.iscte-iul.pt/bitstream/10071/18455/1/CAAT_Adoption_Model_CTWO-D-18-00314R1.pdf [Retrieved On 08.09.2020]

Veitch, R. S., & Seymour, L. F. (2017). Business Process Model Reuse In A Multi-Channel/Multi-Product Environment-Problem Identification And Tentative Design. In MCIS (p. 25). Retrieved from https://core.ac.uk/download/pdf/301373751.pdf [Retrieved On 08.09.2020]